Institutional

Global Implications of U.S. Crypto Regulatory Progress: Post GENIUS & CLARITY Acts

The GENIUS Act and the CLARITY Act give the US its first integrated digital-asset framework, and regulators worldwide are responding. How do MiCA, Hong Kong, Singapore, and the UK compare, and what does the proposed federal carve-out mean for validators?

JUN 05, 2026

Last updated JUL 08, 2026 · V1

TL;DR

- The US has set the global regulatory benchmark for digital assets. The GENIUS Act and the CLARITY Act form the first integrated US digital-asset framework.

- USD-pegged tokens make up for ~99.7% of a $323B+ stablecoin market, foreign regulators respond to US rules rather than opt out.

- The GENIUS Act restricts stablecoin issuance to permitted issuers, splitting the market into permitted-in-US and not-permitted tracks.

- Foreign issuers need Treasury comparability certification plus OCC registration to serve US users.

- The CLARITY Act would settle the SEC-versus-CFTC jurisdiction question for digital assets. For infrastructure providers, it would codify the first federal carve-out confirming that validators and node operators without custody of customer funds are not regulated intermediaries.

- Global regimes (MiCA, HKMA, MAS, UK FCA) share the same prudential pillars: full reserve backing, locally regulated issuer entities, no rewards on balances.

- They diverge on foreign-issuer access and supervision: Hong Kong issued its first 2 licenses on April 10, 2026, and the UK regime goes live on October 25, 2027.

- Staking-as-a-service classification differs under MiCA, the UK FCA regime, MAS rules, and the CLARITY Act, potentially requiring jurisdiction-by-jurisdiction legal mapping.

- This article is intended for informational purposes only. It does not constitute legal or financial advice.

Why US Regulation Matters Globally

The US framework may often dictate terms for a market where US-domiciled actors and US-dollar instruments hold structural dominance. Foreign regulators are unlikely to opt out.

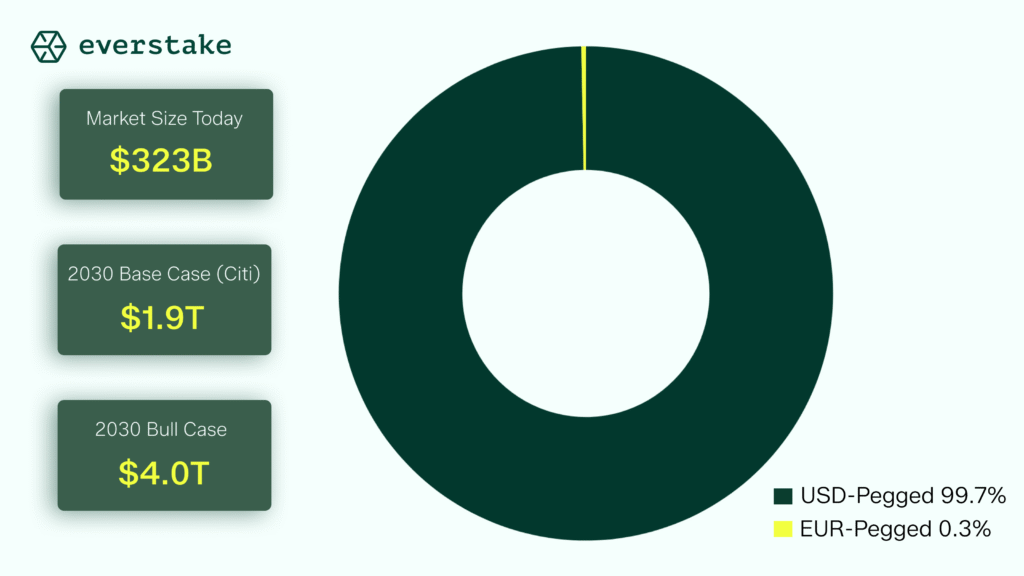

USD-pegged stablecoins represent roughly 99.7% of global stablecoin supply, with Euro-pegged tokens at 0.3% of a market that has surpassed $323 billion in aggregate size.

Major issuers, including:

- Circle (USDC)

- Paxos (USDP, PYUSD)

- JPMorgan (JPMD)

- BlackRock‘s tokenized BUIDL fund (used as reserve collateral)

are US-domiciled and now bound by GENIUS Act rules.

Stablecoin trading volume reached approximately $23 trillion in 2024, per IMF reporting. Citigroup projects total stablecoin issuance of $1.9 trillion in a base case and up to $4.0 trillion in a bull case by 2030.

Extraterritorial sanctions amplify this further. Any foreign bank, exchange, or asset manager touching a US-issued stablecoin is in scope of the OFAC seize-freeze-burn requirements baked into GENIUS.

GENIUS Act Overview and Provisions

Signed by President Trump on July 18, 2025, the Guiding and Establishing National Innovation for U.S. Stablecoins Act (S. 1582) cleared the Senate 68–30 on June 17, 2025, and the House 308–122 on July 17, 2025. The act becomes effective the earlier of 18 months after enactment or 120 days after final implementing regulations.

The framework limits payment-stablecoin issuance to three permitted-issuer pathways:

- Insured depository institutions and their subsidiaries

- Federally chartered non-bank issuers approved by the OCC

- State-licensed issuers under regimes certified as “substantially similar” to the federal regime, available only for issuers with consolidated issuance of $10 billion or less

Core prudential requirements include 100% backing in high-quality liquid assets (cash, short-dated US Treasuries, repos), monthly public reserve attestations, mandatory redemption at par, and Bank Secrecy Act compliance. The Hagerty Amendment added data-sharing and anti-tying restrictions and granted stablecoin holders priority status in issuer insolvency.

The GENIUS Act establishes a $10 billion consolidated-issuance threshold above which a stablecoin issuer must transition from state to federal supervision.

Importantly, GENIUS prohibits issuers from paying rewards on payment stablecoins. It also forbids misleading claims of US-government backing or federal deposit insurance.

GENIUS Act Implications

The lead implication is bifurcation of the global stablecoin market into permitted-in-US and not-permitted-in-US tracks.

Tether (USDT), the largest stablecoin by issuance, has not registered under GENIUS and remains outside the permitted-issuer perimeter for direct US issuance. Circle, Paxos, and bank-issued products are positioned as compliant alternatives. Tokenized money-market funds such as BlackRock‘s BUIDL, Franklin Templeton‘s BENJI, and WisdomTree‘s WTGXX are eligible reserve collateral subject to attestation rules.

Foreign issuers can serve US users only if they:

- Are domiciled in a jurisdiction the Treasury Secretary certifies as having a comparable regulatory regime

- Register with the OCC

- Hold US-customer reserves in a US financial institution

- Demonstrate technical capability to comply with US lawful orders, including asset freezes

For most non-US issuers, the practical effect is exclusion from the US payment-stablecoin market unless they recharter or operate through a US-licensed affiliate.

CLARITY Act Overview and Provisions

The Digital Asset Market Clarity Act of 2025 (H.R. 3633) addresses the long-standing securities versus commodities question for non-stablecoin digital assets.

Under CLARITY, jurisdiction splits along functional lines:

- The SEC retains primary-market fundraising activity, contract-based asset sales characterized as securities, and continuing anti-fraud authority over assets traded on SEC-registered venues

- The CFTC gains exclusive spot-market authority over “digital commodities” traded on or through new registered entities

The act creates three new CFTC registration categories: digital commodity exchanges (DCEs), digital commodity brokers (DCBs), and digital commodity dealers (DCDs). An expedited registration pathway must open within 270 days of enactment, with 180-day provisional registration windows allowing firms to operate while final rules are written. Provisional status sunsets after four years.

A separate decentralization test governs when a token can graduate from a security to a digital commodity classification. The bill also includes explicit safe harbors for:

- Validators

- Node operators

- Non-custodial wallet software

- Other infrastructure participants that do not control customer funds

The CLARITY Act explicitly excludes validators and node operators from registration requirements, codifying for the first time a US federal carve-out for proof-of-stake infrastructure participants such as those operated by Everstake on Ethereum, Solana, Cosmos, and other networks.

CLARITY Act Implementation Status and Timeline

As of June 2026, the Senate Banking Committee has advanced CLARITY by a 15–9 bipartisan vote. The bill still needs:

- Reconciliation with the version cleared by the Senate Agriculture Committee in January 2026

- Resolution of a contested ethics provision relating to executive-branch officials

- A full Senate floor vote requiring 60 votes for cloture

- House concurrence on the final reconciled text

The most likely passage window is Q3 2026, though TD Cowen analysts have flagged risk of slippage to 2027 given the November 2026 elections. Once enacted, SEC and CFTC rule-making proceeds in parallel, with the expedited registration window opening within 270 days. Legal review is required for any operational planning premised on a specific passage date.

For more in-depth angle check out our previous material, specifically comparing GENIUS Act vs CLARITY Act.

European Response: MiCA Compared

The EU‘s Markets in Crypto-Assets Regulation (MiCA, Regulation (EU) 2023/1114) entered into force for stablecoins on 30 June 2024 and for crypto-asset service providers on 30 December 2024. The statutory review is scheduled for 2026.

MiCA and GENIUS converge on key prudential pillars: full reserve backing, locally regulated issuer entities, segregation and bankruptcy remoteness of reserves, and a prohibition on paying rewards on payment stablecoins. They diverge on scope and supervision.

MiCA covers a broader perimeter, regulating asset-referenced tokens (ARTs), e-money tokens (EMTs), and crypto-asset services across all 27 EU member states, as well as Iceland, Liechtenstein, and Norway. GENIUS addresses payment stablecoins only.

MiCA assigns supervision to a single national competent authority per member state, with passporting across the bloc. GENIUS operates a dual federal-and-state model.

To get a validator’s angle, check out our deep-dive article into MiCa for Staking.

Stablecoin Framework Comparison

| Dimension | GENIUS Act (US) | MiCA (EU) | HKMA (Hong Kong) | FCA (UK, from Oct 2027) |

| In force | July 18, 2025 (effective by Jan 2027) | 30 June 2024 (stablecoin titles) | August 1, 2025 | October 25, 2027 |

| Scope | Payment stablecoins | ARTs, EMTs, broader crypto perimeter | Fiat-referenced stablecoins | Qualifying stablecoins and cryptoassets |

| Reserve backing | 100% in cash, T-bills, repos | 100%, with a bank-deposit floor for ARTs | 100% in high-quality liquid assets | 100% plus issuer-must-be-UK rule |

| Rewards on balances | Prohibited | Prohibited | Prohibited | Under consultation |

| Foreign-issuer access | Comparable-regime certification plus OCC registration | Pre-authorization, EU establishment | License or recognition required | UK establishment required |

| Supervisor | OCC, federal banking agencies, state regulators | National competent authority plus EBA, ECB | HKMA | FCA, Bank of England (systemic) |

| Issuance cap | None | EMT issuer rules with a EUR 200M daily-transaction threshold | License-by-license | TBD |

Asia: Hong Kong, Singapore, and Japan

Asian regulators have not waited for CLARITY to pass before building their own frameworks.

- Hong Kong‘s Stablecoins Ordinance took effect on August 1, 2025. The HKMA received 36 applications and awarded the first two licenses on April 10, 2026, to HSBC and Anchorpoint Financial, a Standard Chartered-led joint venture that includes Animoca Brands. The minimum paid-up funding requirement is HK$25 million (approximately US$3.2 million). Travel-rule reporting applies to transfers above HK$8,000.

- Singapore‘s Monetary Authority of Singapore (MAS) finalized its Digital Token Service Provider framework with rules effective 30 June 2025. The regime sets full reserve, redemption, and disclosure requirements for single-currency stablecoins pegged to the Singapore dollar or any G10 currency.

- Japan‘s Financial Services Agency (FSA) operates a stablecoin regime under the Payment Services Act, restricting issuance to licensed banks, trust companies, and registered money-transfer agents. MUFG, Mitsubishi UFJ Trust, and consortium issuers have moved earliest.

- Each Asian regime aligns with GENIUS on full reserve backing and the prohibition of rewards on payment stablecoins. They diverge on foreign-issuer treatment and on whether a CBDC complements or competes with private stablecoins.

UK and Emerging-Market Responses

The UK‘s Financial Conduct Authority released finalized cryptoasset perimeter guidance in April 2026, with the consultation closing 3 June 2026. The full authorization regime goes live on 25 October 2027, and the application gateway opens in September 2026 with a five-month window.

Key UK features include:

- A mandatory UK establishment requirement for qualifying stablecoin issuers

- Custody triggered for any firm holding client cryptoassets for more than 24 hours

- Validator and node-operator carve-outs where activity is genuinely technical

- A separate Bank of England regime for stablecoins deemed systemic

The Transatlantic Taskforce for Markets of the Future, co-chaired by HM Treasury and the US Treasury with participation from the FCA, SEC, CFTC, and Bank of England, was established during President Trump‘s September 2025 state visit and held its first senior-level engagement in London on 26 January 2026.

Emerging-market responses vary. Brazil aligns closer to MiCA. Mexico restricts retail stablecoin products at supervised banks. The UAE VARA and ADGM regimes remain open. Nigeria, the Philippines, and Argentina host the largest dollarized stablecoin user bases and have prioritized AML rules over issuance bans.

Central Bank Reactions and CBDC Implications

The Bank for International Settlements (BIS) has flagged dollar-denominated stablecoin growth as a financial-stability and monetary-sovereignty risk for non-US jurisdictions and has called for cross-border supervisory cooperation.

The European Central Bank has accelerated work on the digital euro, with ECB President Christine Lagarde stating publicly that the GENIUS Act is being used as an instrument to reinforce dollar dominance and demand for US Treasuries. ECB sources have indicated openness to public-blockchain settlement layers, including Ethereum and Solana, for digital-euro distribution under controlled conditions.

The People’s Bank of China continues its e-CNY rollout while maintaining a prohibition on private stablecoins on the mainland. Hong Kong is the explicit exception, operating as a sandbox for offshore Renminbi tokenization through licensed bank issuers.

The Federal Reserve maintains a no-retail-CBDC stance under the current administration, by design ceding the digital-dollar function to regulated private issuers under GENIUS. Treasury Secretary Scott Bessent has framed stablecoin growth as supportive of US Treasury demand.

For non-US central banks, the strategic question is whether to compete (digital euro, e-CNY, Project mBridge), regulate (MiCA, HKMA, MAS), or accommodate (UAE, several emerging markets).

Cross-Border Flows and Corridor Impact

When it comes to staking for global asset managers, the corridors most affected by GENIUS Act restrictions are those where USD stablecoins have displaced traditional remittance and trade-settlement rails:

- US-LATAM: Remittances to Mexico, Colombia, Brazil, and Argentina, where stablecoin payouts have grown substantially

- US-Asia: Trade settlement, B2B treasury, and Philippines and Indonesia remittance flows

- EU-Africa: EU-domiciled fintechs serving Nigeria, Kenya, and Ghana through USD stablecoin pipes

- Intra-Asia: Hong Kong, Singapore, and the UAE corridors are increasingly served by licensed local stablecoins

GENIUS‘s foreign-issuer restrictions do not directly prohibit non-US users from holding US-issued stablecoins. They may restrict the issuance perimeter. Non-US holders of USDC, PYUSD, or bank-issued USD stablecoins remain bound by the lawful-order framework and reserve protections built into the act.

FATF-aligned travel-rule harmonization continues separately. MiCA‘s transfer-of-funds regulation, the HKMA HK$8,000 threshold, and the US $3,000 FinCEN threshold remain non-harmonized, complicating cross-border compliance.

Potential Impact on Validators

Validator infrastructure on public proof-of-stake networks (Ethereum, Solana, Cosmos, NEAR) carries the cross-border stablecoin and tokenized-asset volume affected by these regulations.

Everstake operates validator nodes on more than 130 networks and supports institutional staking and custodian-integrated staking. Everstake monitors regulatory developments in the jurisdictions relevant to its operations and aligns its practices with evolving requirements as they take effect.

The CLARITY Act validator carve-out, if enacted, would for the first time provide US federal-statute clarity that transaction validation is not a regulated activity.

Independently audited operational controls and information-security certifications have become baseline expectations when institutional counterparties evaluate validator and infrastructure providers.

Everstake maintains a compliance and information-security program designed to meet institutional requirements. Current certification details are available from the Everstake information-security and compliance team.

For staking-as-a-service classification, MiCA, the UK FCA, and MAS all treat the activity differently from CLARITY‘s proposed approach, creating a multi-regime compliance burden that legal counsel must map for each operating jurisdiction. Legal review required.

What to Watch in 2026 to 2027

A short list of milestones that will define the next 18 months:

- CLARITY Act final passage and signing, most likely in Q3 or Q4 2026

- SEC and CFTC joint rule-making, including the digital-commodity definition, decentralization test, and DCE, DCB, DCD registration rules

- GENIUS Act Treasury and federal-banking-agency rule-making, due within one year of enactment (by July 2026)

- GENIUS Act effective date, the earlier of 18 months post-enactment or 120 days after final regs

- MiCA statutory review and any EU legislative response in 2026

- UK full regime go-live on 25 October 2027, with the application gateway opening September 2026

- HKMA second and third waves of stablecoin licenses

- FATF guidance updates on agentic and DeFi flows, plus sanctions enforcement priorities

Operational planning that depends on any single milestone should be stress-tested against a 2027 slippage scenario. Legal review required.

FAQ

Does the GENIUS Act ban Tether?

No. The act restricts US issuance to permitted issuers. USDT itself is not issued by a US-licensed entity, and Treasury has not yet granted the foreign-issuer equivalency determination it would need. That review is ongoing within the act’s transition window.

Can foreign stablecoins operate in the US?

Yes, but only if the issuer is domiciled in a jurisdiction the Treasury Secretary certifies as having a comparable regime, registers with the OCC, holds US-customer reserves in a US financial institution, and complies with US lawful orders.

How does the GENIUS Act compare to MiCA?

Both require full reserve backing and prohibit rewards on payment stablecoins. MiCA covers a broader scope, uses a single-supervisor model per member state with passporting, and caps certain EMT transaction volumes. GENIUS is narrower (payment stablecoins only) and uses a dual federal-and-state model with no issuance cap.

When does the CLARITY Act take effect?

It is not a law yet. The bill cleared the Senate Banking Committee 15–9 on May 14, 2026, and was placed on the Senate Legislative Calendar on June 1 a floor vote, House reconciliation, and presidential signature remain. Likely passage: H2 2026, with rules phasing in through 2027.

Do tokenized money-market funds qualify under the GENIUS Act?

Tokenized MMFs may serve as eligible reserve assets for permitted issuers, subject to attestation, custody, and liquidity rules. They are not themselves payment stablecoins, and continue to be regulated as registered fund securities under existing US federal fund-regulation statutes.

What is the impact on non-US users?

Non-US users may continue to hold and use US-issued stablecoins. The act’s primary effect is indirect: stronger reserve protections, mandatory redemption rights, freeze-and-seize capability tied to US lawful orders, and reduced availability of non-compliant USD stablecoins over time.

How does the CLARITY Act treat validators and stakers?

Validating transactions and running nodes are explicitly excluded from intermediary-registration requirements where the activity does not involve custody of customer funds. Staking-as-a-service classification depends on whether/if the provider takes custody or directs allocation of staked assets.

Disclaimer

This document is provided for informational purposes only. It does not constitute legal, tax, financial, or investment advice, and nothing contained herein should be construed as such. The information presented reflects publicly available sources as of the date of publication and is subject to change as regulatory frameworks, legislation, and market conditions evolve.

Readers should not rely on this document as a basis for any legal, tax, financial, or business decision. All operational, compliance, and strategic decisions should be made only after obtaining advice from qualified legal counsel, tax advisors, financial advisors, or other relevant professionals with expertise in the applicable jurisdictions and subject matter.

Share with your network