The ABCs of Crypto

Stablecoins Explained: The New Era for Value Transfer

Stablecoins peg digital tokens to fiat or other assets to deliver predictable value alongside blockchain speed and programmability. Their stability depends on collateral models, validator infrastructure, and frameworks like MiCA, with new formats now emerging.

MAR 06, 2026

Last updated MAY 11, 2026 · V1

TL:DR

- Stablecoins are digital tokens pegged to traditional assets like the US Dollar, combining the speed, borderless nature, and programmability of cryptocurrency with predictable fiat value.

- Everstake examines how stablecoins work, the validator infrastructure that secures them, and what enterprises should know in 2026.

Key facts to know:

- They settle trillions of dollars in annual volume.

- The four main models are fiat-backed, crypto-collateralized, algorithmic, and yield-bearing.

- Europe’s MiCA framework requires 1:1 liquid reserves.

- Validator uptime of 99.9% is the institutional benchmark.

What Stablecoins Are and Why They Matter

Stablecoins are digital tokens that are designed to maintain a constant price. They serve as the foundational liquidity layer for the digital economy.

Before stablecoins, converting crypto back to fiat to escape volatility was slow and expensive. Today, stablecoins facilitate trillions of dollars in annual settlement volume, serving as safe havens during market turbulence, as the backbone of DeFi, and, increasingly, as a preferred medium for cross-border B2B payments.

How Stablecoins Work

To maintain a consistent value (the “peg”), stablecoin issuers must balance supply and demand through specific mechanical loops.

When a user wants fiat-backed stablecoins, they deposit fiat currency with the issuer. The issuer then mints (creates) an equivalent amount of stablecoins on the blockchain and sends them to the user.

When the user wants their fiat back, they return the stablecoins to the issuer, who burns (destroys) the digital tokens and wires the fiat back to the user’s bank account.

This mechanism relies heavily on arbitrage. If a stablecoin trades at $0.99 on a cryptocurrency exchange, traders will buy it at a discount, redeem it with the issuer for a full $1.00, and pocket the difference.

This buying pressure pushes the exchange price back up to $1.00.

Types of Stablecoins

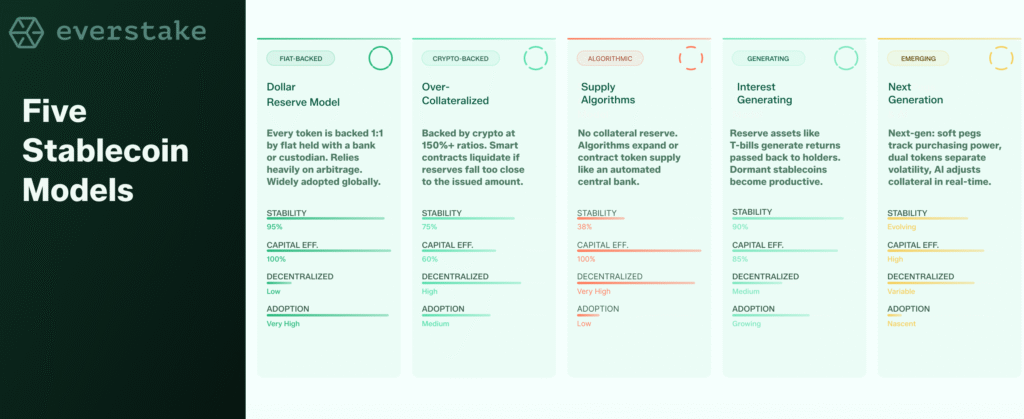

Stablecoins fundamentally differ in how they collateralize their assets to maintain the peg. The four main models each carry distinct risk and capital-efficiency trade-offs.

Fiat-Backed

The most straightforward and widely used model. In it, for every digital token issued, the equivalent amount of fiat currency (in most cases) is held in a regular bank account or a custodian.

Crypto-Collateralized

Instead of traditional bank reserves, these stablecoins are backed by other cryptocurrencies. Because crypto is volatile, these are over-collateralized.

For example, to mint $100 of a crypto-backed stablecoin, a user might need to lock up $150 worth of Ethereum in a smart contract. If the collateral’s value drops too close to the issued amount, the smart contract automatically liquidates it to protect the peg.

Algorithmic

Algorithmic stablecoins do not rely on a collateral reserve. Instead, they use smart contract algorithms to expand or contract the supply of tokens in response to market demand, acting somewhat like an automated central bank.

While highly capital-efficient, these stablecoins have proven highly susceptible to “death spirals” if market confidence breaks.

Yield-Bearing and Hybrid Models

With traditional interest rates remaining relevant, users want their dormant digital cash to work for them. Yield-bearing stablecoins take reserve assets (such as Treasuries or collateralized debt) and pass the generated interest directly back to token holders.

Hybrid models may mix fiat reserves, crypto over-collateralization, and algorithmic stabilization to optimize capital efficiency while mitigating risk.

Emerging Models (Soft Pegs, Dual Token, AI-assisted)

The next generation of stable-value assets is experimenting with three approaches:

- Soft pegs: assets that don’t track $1.00 exactly, but instead track purchasing power or a basket of goods.

- Dual-token systems: separating the stable value from the volatility-absorbing token.

- AI-assisted dynamic collateralization: where machine learning adjusts collateral ratios in real-time based on predictive market risk models.

Stablecoins in the Global Financial System

Payments and Treasury Use

Multinational enterprises are using stablecoins for treasury management and global payroll. Traditional cross-border wire transfers (SWIFT) can take days and often involve high fees, particularly in emerging markets.

Stablecoin settlements settle in seconds for minimal fees and operate 24/7 all year round.

Monetary Policy and CBDCs

Central Bank Digital Currencies (CBDCs) are the government’s answer to privately issued stablecoins. While CBDCs offer the ultimate fiat guarantee, they raise concerns regarding state surveillance and control over personal finance.

Heavily regulated private stablecoins are currently out-competing CBDC pilots by leveraging open-source blockchain infrastructure.

The Infrastructure Behind Stablecoins: Why Validators Matter

Validators act as the system’s backbone, maintaining the blockchain networks (like Ethereum, Solana, or Polygon) where stablecoins live and move.

How Validators Secure Stablecoin Transactions

In Proof-of-Stake networks, validators verify and batch stablecoin transfers into blocks and ensure stability and security of the entire network. They are required to “stake” their own cryptocurrency as collateral to guarantee honest behavior.

Without a decentralized and secure set of validators, the underlying network could be compromised, putting the billions of dollars in stablecoins traversing it at risk.

Validator Performance and Transaction Finality

For enterprise stablecoin use, transaction finality (the exact moment a payment cannot be reversed) is critical. High-performing validators ensure networks run fast and without dropped blocks, making stablecoins viable for high-frequency trading and point-of-sale retail transactions.

What Enterprises Should Look for in a Validator Partner

When institutions launch their own stablecoins or stake treasury assets, they need enterprise-grade validator partners. Key criteria include:

- Geographic and cloud-provider decentralization to avoid single points of failure.

- SOC 2 compliance and institutional-grade security.

- Hardware redundancy and 24/7 engineering support.

Slashing, Uptime, and Risk Management

If a validator acts maliciously or goes offline for extended periods, the network penalizes them by slashing (destroying a portion of their staked collateral). Reliable validators employ stringent risk management and backup nodes to ensure 99.9%+ uptime, protecting the institutional capital that relies on their infrastructure.

Regulatory Approach Around the World

Regulatory clarity has become a crucial catalyst for stablecoin adoption. Three regions illustrate the global picture:

- Europe: The MiCA (Markets in Crypto-Assets) framework provides the clearest rules globally, requiring stablecoin issuers to hold 1:1 liquid reserves and obtain e-money licenses.

- United States: The landscape remains fragmented among the SEC, the CFTC, and various state regulators, though legislative efforts (such as the Clarity for Payment Stablecoins Act) aim to establish a unified federal framework.

- Asia-Pacific: Jurisdictions such as Singapore (MAS) and Hong Kong have established strict and clear taxonomies, heavily favoring fully backed, audited fiat models to protect retail users.

Enterprise Adoption Challenges

Despite the benefits, large-scale corporations face hurdles in integrating stablecoins into their legacy systems.

Security and Custody

Self-custodying digital bearer assets is risky. Enterprises must integrate with qualified institutional custodians that use Multi-Party Computation (MPC) or hardware security modules to securely manage private keys.

Transparency and Auditability

Connecting real-world accounting software with on-chain data is technically complex. Enterprises need reliable oracle and API integrations to demonstrate to auditors that on-chain holdings exactly match off-chain liabilities.

Privacy and Competitive Risks

Public blockchains are radically transparent. A competitor could theoretically view an enterprise’s stablecoin wallet to deduce their supply chain partners, payroll size, or treasury strategy.

Zero-knowledge proofs (ZKPs) and private subnets are being actively developed to address this confidentiality gap.

Market Data and Trends

As of early 2026, the stablecoin market continues to mature at a measurable pace. High traditional interest rates have accelerated the growth of yield-bearing stablecoins, forcing legacy issuers to innovate.

While Ethereum remains the dominant layer for high-value settlement, networks like Solana, Tron, and various Layer-2 rollups are capturing volumes of micro-transactions and retail remittances due to their near-zero fees.

The New Standard of Value

Stablecoins are a fundamental upgrade to the architecture of global finance. They merge the stability of traditional money with the cryptographic security and speed of blockchain validators, paving the way for a more accessible, programmable, and efficient economy.

FAQ

What is a stablecoin and how does it maintain its price?

A stablecoin is a digital token designed to hold a constant price, most often pegged to the US Dollar.

What are the main types of stablecoins?

There are four primary categories. Fiat-backed stablecoins hold traditional currency 1:1 in a bank or custodian account. Crypto-collateralized stablecoins lock other cryptocurrencies in a smart contract and are over-collateralized, for example $150 of ETH to mint $100 of stablecoin. Algorithmic stablecoins use smart contracts to expand or contract supply without reserves, and yield-bearing or hybrid models pass interest from reserve assets like Treasuries back to holders or blend several mechanisms together.

Why do enterprises use stablecoins?

Traditional SWIFT wire transfers can take days and carry high fees, particularly in emerging markets. Stablecoin settlements clear in seconds for marginal fees and run 24/7 across any time zone.

What role do validators play in the stablecoin ecosystem?

Validators secure the Proof-of-Stake networks like Ethereum, Solana, and Polygon where stablecoins move. They verify and batch stablecoin transfers into blocks.

Which blockchains are stablecoins most active on?

Ethereum currently remains the dominant network for high-value settlement. Solana, Tron, and various Layer-2 rollups capture large volumes of micro-transactions and retail remittances thanks to near-zero fees.

Disclaimer:

Everstake acts solely as a technical provider. Everstake does not engage in the provision of advice, portfolio management, brokerage services, custody of client funds, or any other regulated service, does not perform any regulated brokerage or dealing services, does not act as a fiduciary, agent, advisor, or representative authorized to act on behalf of the users.

Share with your network