Institutional

Atomic Settlement and T+0 Explained: How Blockchain Replaces Legacy Clearing

Learn how atomic settlement collapses the multi-day T+2 cycle into a single on-chain transaction, eliminating counterparty risk, margin collateral, and reconciliation overhead. Why banks like JPMorgan, Goldman Sachs, and Citi are building compliant on-chain cash, what the compliance stack requires, and how CFOs and treasury teams should evaluate settlement infrastructure.

APR 28, 2026

Last updated APR 28, 2026 · Vv1.

Key Takeaways

Atomic settlement is an all-or-nothing exchange. Both the asset and the payment move in a single on-chain transaction. If one leg fails, neither side changes hands. There is no counterparty risk window, no escrow intermediary, and no multi-day wait.

- It fixes the structural lag in legacy markets. Traditional T+2 settlement locks billions in margin collateral, exposes both parties to default risk for 48+ hours, and forces costly reconciliation across fragmented intermediaries. Atomic settlement collapses that entire cycle into seconds.

- The cash leg is currently the bottleneck. A tokenized asset can move on-chain in moments, but if the corresponding payment still travels through traditional banking rails, the transaction cannot be truly atomic. On-chain settlement only works end-to-end when both the asset and the cash exist on the same ledger.

- Banks are now issuing on-chain money that complies. JPMorgan’s JPM Coin is live on Base and Canton. A 9-bank consortium including Goldman Sachs, Bank of America, and Citi is building a joint G7-currency stablecoin. These bank-issued deposit tokens bring regulated, KYC-compliant cash to the blockchain, closing the gap that private stablecoins alone could not fill for institutional use.

- Businesses face real operational consequences. Faster settlement frees trapped capital, removes reconciliation overhead, enables 24/7 transaction finality, and opens access to tokenized asset classes like bonds, equities, and real-world assets. CFOs and treasury teams that ignore this shift risk operating on infrastructure their counterparties have already moved beyond.

- None of this works without a reliable infrastructure. Atomic settlement depends on validators and nodes that process blocks without interruption. A missed attestation or a network outage during settlement results in a failed trade. Enterprise-grade uptime, geographic redundancy, and compliance-ready node operations are the foundation on which the entire model rests.

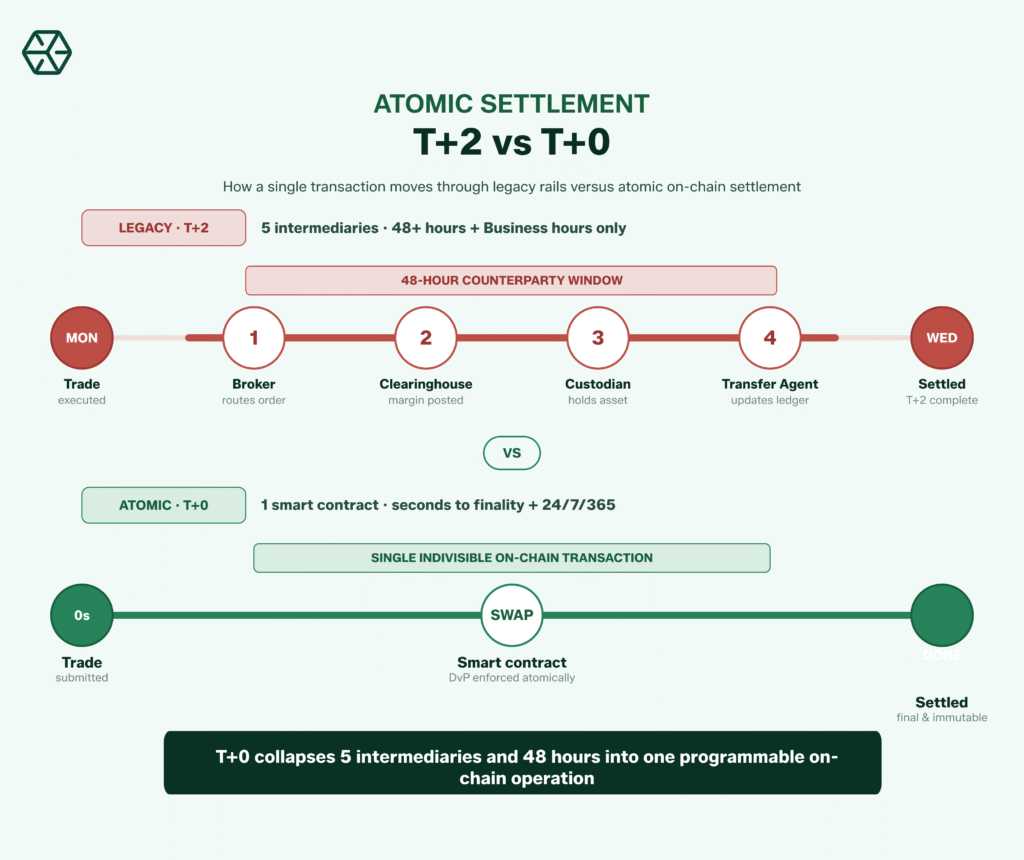

Atomic settlement eliminates the gap between trade execution and final ownership transfer. In legacy markets, a stock purchased on Monday may not officially change hands until Wednesday. Blockchain settlement compresses that into a single programmable operation.

The Settlement Problem: Why T+2 Is a Systemic Inefficiency

Traditional securities markets still operate on a T+2 cycle across much of Europe. The “T” stands for trade date, and the number indicates the number of business days before the transaction is final. During those 2 days, neither the buyer’s cash nor the seller’s securities are truly committed, and both sides face default risk.

Clearinghouses absorb that risk by demanding margin deposits. During the GameStop volatility in January 2021, the NSCC issued emergency margin calls that forced Robinhood to post an additional $3 billion in collateral in a single morning. Other brokerages lacked the liquidity to meet similar demands, leading to restricted buy orders and market paralysis.

The U.S. move from T+2 to T+1 (effective May 2024) helped. The NSCC reported a roughly 30% decrease in its clearing fund, freeing approximately $3.7 billion from collateral obligations. But T+1 still leaves a full business day of counterparty risk, and Europe remains on T+2, aiming to move to T+1 by October 2027. The core inefficiency is structural: multiple intermediaries (custodians, central counterparties, registrars, transfer agents) each maintain their own ledger and reconcile at the end of each day. Accenture estimates that distributed ledger technology could reduce post-trade clearing and settlement costs by up to 50%.

T+0 vs T+2: Side-by-Side Comparison

| Feature | T+2 Settlement | T+0 (Atomic) Settlement |

| Speed | 2 business days after trade | Seconds to minutes, same transaction |

| Counterparty risk | Open for 48+ hours, margin required | Eliminated at execution, both legs settle, or neither does |

| Efficiency | Billions locked in margin and collateral | Funds are freed immediately, no margin buffer needed |

| Infrastructure | DTCC, CCP, custodians, transfer agents | Smart contracts, on-chain ledger, tokenized cash |

| Audit trail | Fragmented across multiple databases | Single immutable record on a shared ledger |

| Operating hours | Business hours only (weekdays) | 24/7/365 continuous availability |

| Reconciliation | End-of-day batch processing across systems | Real-time, single source of truth |

| Error handling | Manual correction over days | Transactions are complete fully or revert automatically |

What Is Atomic Settlement?

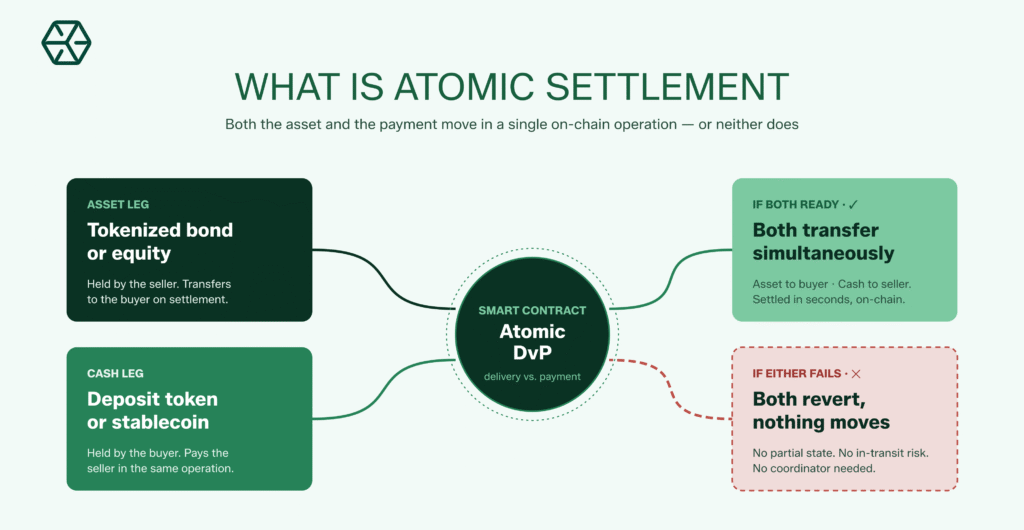

Atomic settlement is a mechanism where both legs of a transaction, asset delivery and cash payment, execute as a single indivisible operation. The word “atomic” comes from the Greek atomos, meaning “uncuttable.”

The smart contract governing the trade enforces an all-or-none condition: if the buyer’s tokenized cash and the seller’s tokenized asset are both available, both are transferred simultaneously. If either condition fails, neither party’s position changes.

This contrasts with the traditional delivery-versus-payment (DvP) model, where “versus” implies two separate processes coordinated but not truly unified.

Legacy DvP relies on intermediaries to ensure both sides follow through. On-chain settlement removes this coordination problem.

A single blockchain transaction either succeeds in full or fails in full, with no partial state, no in-transit period, and no window for one party to receive value while the other waits.

Why Banks Are Building Blockchain Settlement (BofA, Citi, Goldman)

In May 2025, The Wall Street Journal reported that JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo were in active discussions about launching a joint stablecoin. By October 2025, a broader consortium had formed: Goldman Sachs, Deutsche Bank, Barclays, Bank of America, BNP Paribas, Citigroup, MUFG, TD Bank Group, UBS, and Banco Santander announced plans to develop a jointly backed stablecoin pegged to G7 currencies.

For blockchain settlement to work at an institutional scale, the cash leg must live on the same ledger as the asset leg.

Without a bank-grade digital dollar on-chain, the “atomic” part of atomic settlement breaks down because one leg still passes through the traditional banking system.

Citi’s CEO, Jane Fraser, stated during Q2 2025 that Citi is “very active” in the tokenized deposit space. Citi also joined a European stablecoin consortium in October 2025 as the only non-European bank in the group, and a Citi GPS report described 2025 as blockchain’s “ChatGPT moment” for institutional adoption.

Private stablecoins issued by companies like Circle and Tether already process trillions of dollars in annual volume. Banks risk being disintermediated from the settlement layer if they do not build their own on-chain cash instruments.

Named Examples: JPM Coin, Project Guardian, and Others

JPM Coin (JPMD) by JPMorgan

JPM Coin is the first bank-issued U.S. dollar deposit token. Conceptualized in 2019, it rolled out to institutional clients on Coinbase’s Base (Ethereum Layer 2) in November 2025 and expanded to the Canton Network in January 2026. It represents a direct claim on deposits held at JPMorgan and operates only with whitelisted wallets, subject to full KYC controls.

Project Guardian (Monetary Authority of Singapore)

Project Guardian MAS is an international initiative that brings together policymakers, banks, and market infrastructure providers to explore the potential of asset tokenization. In 2025, it published a DvP settlement guide for DLT-based debt securities and an operational roadmap for tokenized funds. The ICMA leads the bond markets workstream, while a July 2025 report by ISDA and Ant International proposed principles for tokenized bank liabilities in FX settlement, with contributions from BNY, HSBC, and OCBC.

Project Agora (Bank for International Settlements)

Project Agora unites 7 central banks (including the Federal Reserve Bank of New York, the Bank of England, and the Bank of Japan) with over 40 private institutions to build a multi-currency, unified ledger. It entered testing in early 2026. A key design goal is to embed compliance checks at payment origination and share them across institutions, targeting redundant AML/KYC screening as the primary source of cross-border delays.

DTCC Tokenization Pilot

In December 2025, the SEC issued a no-action letter permitting DTC (a DTCC subsidiary) to operate a 3-year tokenization pilot covering equities, ETFs, corporate bonds, and U.S. Treasuries. Launching in the second half of 2026 on the Canton Network, the pilot allows security entitlements to be recorded on a distributed ledger and transferred between registered wallets at any time, including outside standard operating hours.

The Compliance Stack: What Makes Settlement Compliant

On-chain settlement does not eliminate regulatory obligations. The compliance stack for tokenized settlement rests on several pillars.

- KYC (Know Your Customer). Every participant must be identified and verified before network access is granted. JPM Coin operates exclusively with whitelisted wallet addresses tied to onboarded institutional clients, replicating the controls central counterparties enforce in traditional markets.

- AML (Anti-Money Laundering). Because every transaction is recorded on a shared ledger, compliance teams can screen flows in real time rather than reconciling batch reports across databases. Project Agora explicitly targets redundant AML checks by sharing compliance data at origination.

- Auditability. Blockchain creates a permanent audit trail with timestamps and cryptographic verification, allowing regulators to inspect it without requesting data from multiple institutions.

- ISO 20022 compatibility. SWIFT completed its ISO 20022 cutover in November 2025. Blockchain platforms that support ISO 20022-structured data can communicate natively with legacy payment rails, ensuring that tokenized transactions carry the structured metadata that regulators expect.

- Regulatory frameworks. Settlement finality must be legally anchored. Project Guardian’s roadmap notes that finality on a distributed ledger cannot depend solely on probabilistic consensus. The DTCC pilot requires DTC to retain override capabilities through a “root wallet” for legally mandated corrections.

How to Evaluate a Settlement Infrastructure

For CFOs, treasury managers, and RWA protocol builders assessing platforms, focus on operational viability.

- Settlement finality and legal certainty. Does the platform define when a transaction becomes legally irreversible? Look for deterministic finality mechanisms and supporting legal opinions.

- Compliance integration. Does the system support KYC/AML at the protocol level? Permissioned access, real-time monitoring, and sanctions screening are baseline requirements.

- Cash leg availability. Evaluate whether the platform supports bank-issued deposit tokens, regulated stablecoins, or wholesale CBDC. A settlement system without compliant on-chain cash is incomplete.

- Interoperability. Cross-chain messaging, ISO 20022 compatibility, and API integrations with custody and reporting infrastructure prevent assets from becoming trapped on a single chain.

- Infrastructure reliability. Evaluate uptime SLAs, geographic distribution, and redundancy architecture. Validator and node performance directly affects whether settlement completes on time.

- Governance. Who controls upgrades? How are disputes resolved? Institutional participants need transparent governance and documented change management.

Everstake: Infrastructure for Institutional and RWA Chains

Validator reliability is settlement reliability. When a tokenized bond settles through a smart contract, the transaction depends on blockchain nodes processing blocks without interruption. A validator that goes offline or misses attestations can delay settlement at the protocol level.

Everstake operates validator infrastructure across more than 30 proof-of-stake networks, serving over 735 thousand delegators. Its bare-metal servers are distributed across Tier III/IV data centers, maintaining 99.98% uptime. Everstake is the only validator operator certified across SOC 2 Type II, ISO/IEC 27001, NIST CSF 2.0, ITGC, GDPR, and CCPA.

Everstake offers non-custodial Validator-as-a-Service (VaaS) with custom SLAs and a history of integrations with BitGo and Anchorage Digital, allowing clients to retain full control of their assets.

Frequently Asked Questions

What is atomic settlement?

Atomic settlement executes both sides of a financial transaction, asset delivery, and cash payment, as a single indivisible on-chain operation. Both legs are completed simultaneously, or neither is, eliminating the counterparty risk window in traditional settlement.

What is T+0 settlement?

T+0 means the transaction settles on the same day (or within seconds) of the trade date. Blockchain-based T+0 uses smart contracts to execute delivery-versus-payment in a single on-chain transaction, eliminating multi-day processing.

How does T+0 compare to T+2 settlement?

T+2 requires 2 business days for ownership transfer, exposing both parties to counterparty default risk. T+0 removes this gap. Practical differences extend to fund efficiency (no margin collateral), operational cost (no multi-party reconciliation), and availability (24/7 versus business hours).

Which banks are building blockchain settlement systems?

JPMorgan launched JPM Coin in November 2025 and expanded it to the Canton Network in January 2026. A consortium including Goldman Sachs, Bank of America, Citigroup, Deutsche Bank, and UBS announced in October 2025 plans for a joint G7-currency stablecoin. The BIS’s Project Agora involves 7 central banks and 40+ financial institutions.

What is bank stablecoin settlement?

Bank stablecoin settlement uses digital tokens issued by regulated banks, backed 1:1 by fiat deposits, to complete the cash leg of on-chain transactions. Bank-issued deposit tokens (such as JPM Coin) represent direct claims on deposits with full regulatory protections, making them suitable for institutional settlement where counterparty trust and legal certainty are required.

Is atomic settlement only for crypto assets?

No. The DTCC’s tokenization pilot covers equities, ETFs, corporate bonds, and U.S. Treasuries. Project Guardian focuses on bond instruments and fund distribution. Atomic settlement applies to any asset that can be represented as a token, including real estate, commodities, and private credit.

Disclaimer:

This guide is provided for informational purposes only and does not constitute legal, financial, tax, or investment advice. The information contained herein reflects the state of applicable regulations and market practices as of the date of publication and is subject to change without notice. Readers should not rely on this material as a substitute for independent professional advice tailored to their specific circumstances.

The regulatory analysis in this guide is provided as general background only. Compliance obligations vary by jurisdiction, entity type, and individual facts. Institutions should consult qualified legal and compliance counsel before making any decisions relating to staking arrangements, custody models, or regulatory status.

The information provided is not intended for recipients residing in the United Kingdom.

Share with your network