ethereum

Ethereum L2 Consolidation 2026:Will Only Base, Arbitrum & Optimism Survive as Institutional Rails?

Arbitrum, Optimism, and Base dominate the Ethereum L2 market in 2026, together handling close to 90% of all L2 transactions. The three chains differ by design: Arbitrum leads in DeFi depth at $15.5B TVS, Base in user volume, and Optimism in modular architecture via the OP Stack.

MAY 22, 2026

Last updated MAY 22, 2026 · V1

Key Takeaways

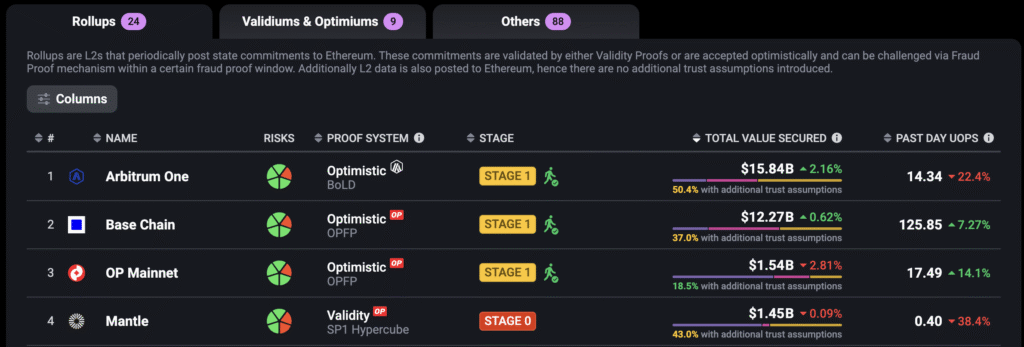

- Arbitrum leads Ethereum L2s in DeFi total value secured (TVS), commanding roughly $15.5 billion and ~38% of L2 DeFi share.

- Base dominates user activity, processing over 37% of all L2 transactions and holding ~30% of L2 DeFi TVS, according to 21Shares data.

- Optimism anchors the OP Stack Superchain, a federation of 30+ chains including Base, Worldchain, Soneium, Unichain, and Kraken’s Ink.

- Robinhood Chain, an Arbitrum Orbit L2, processed 4 million transactions during its first testnet week in February 2026.

- The top three L2s now handle nearly 90% of all L2 traffic, while smaller rollups might face survival risk per 21Shares’ December 2025 report.

The Arbitrum vs Optimism debate now sits inside a three-horse race. Arbitrum, Optimism, and Base are the largest Ethereum Layer 2 networks in 2026, accounting for the majority of L2 transaction volume and TVS.

Arbitrum leads in DeFi depth and institutional rails (including Robinhood’s Arbitrum Orbit chain). Base leads in user growth via Coinbase’s distribution.

Optimism leads in modular architecture through the OP Stack ecosystem (including Kraken’s Ink L2). For most users, the right choice depends on which dApps you use and where liquidity is deepest.

What are Ethereum L2s?

An Ethereum L2 is a separate execution layer that bundles transactions off-chain and posts transaction data back to Ethereum for settlement. This design inherits Ethereum’s security while delivering throughput and fees that the base layer cannot match.

Rollups exist because the Ethereum mainnet processes only about 20-25 transactions per second, with fees that spike during congestion. L2s moved roughly 60–70% of Ethereum activity off-chain by 2026, cutting average transaction costs (compared to Ethereum L1) by 90–99% through batching and the EIP-4844 blob upgrade.

The Ethereum Layer 2 category breaks into several types:

- Optimistic rollups like Arbitrum, Optimism, and Base, which assume validity unless challenged

- Zero-knowledge rollups like zkSync Era and Starknet, which post cryptographic proofs

- Validiums and sidechains, which use alternative security models to achieve lower costs.

The big three optimistic rollups now hold the bulk of secured value. Smaller chains compete for what remains, and many are running on fumes.

Arbitrum: DeFi Depth and Institutional Rails

Arbitrum is the largest Ethereum L2 by TVS, holding around $15.5 billion in DeFi assets in early 2026. Built by Offchain Labs and launched in August 2021, it commands roughly 38% of the L2 DeFi market share.

Major protocols on Arbitrum include:

- Aave (lending)

- Uniswap (DEX)

- GMX (perpetual futures)

- Curve and Pendle (stablecoins and fixed-rate markets)

Composability is the moat. Traders can route, hedge, lend, and collateralize without leaving the chain, which is why so much liquidity sits there.

Arbitrum’s stablecoin balances crossed $5 billion in Oct 2025, and the network ranked at or near the top of all L2s in bridge inflows that year.

The Robinhood Arbitrum integration cemented the chain’s institutional position. Robinhood Chain, built on Arbitrum Orbit, launched its public testnet on February 10, 2026, and processed 4 million transactions during its first week. The chain is purpose-built for tokenized stocks, ETFs, and other real-world assets, with a planned mainnet release later in 2026.

Robinhood committed $1 million to the 2026 Arbitrum Open House developer program, sponsoring buildathons in:

- New York

- Dubai

- London

- Singapore

The technical roadmap covers the ArbOS 51 Dia upgrade, a $215 million gaming catalyst fund, and Stylus multi-language smart contracts. Arbitrum wins by going deeper, not wider.

Optimism: OP Stack and the Modular Ethereum L2 Ecosystem

Optimism holds about $1.5 billion in TVS, but its strategic weight comes from the Superchain thesis. The OP Stack powers a federation of 30+ chains that share security, governance standards, and a communication layer.

Notable Superchain members include:

- Base (Coinbase)

- Unichain (Uniswap)

- Soneium (Sony)

- Worldchain (formerly Worldcoin)

- Ink (Kraken)

The Kraken Ink L2 debuted in December 2024 and grew from $7 million to over $450 million in TVS. It launched with one-second block times, sub-cent fees, and was the first Superchain network to deploy multiple permissionless fault-proof challengers shortly after launch.

The Bedrock architecture made the OP Stack modular and EVM-equivalent, so any Solidity contract on Ethereum can be deployed to Optimism without modification. Optimism’s upcoming Interop Layer, slated for early 2026, aims to make cross-chain message passing among Superchain L2s feel like switching browser tabs rather than bridging.

Base: Coinbase Distribution and Consumer Apps

Base launched in August 2023 on the OP Stack and quickly became the consumer app gravity well of the L2 sector. The chain holds roughly $12 billion in TVS and represents 30% of L2 TVS, while leading all L2s in daily active users.

Base’s edge is the distribution. Coinbase funnels its 120+ million verified users directly onto the chain, solving the cold-start problem that negatively impacts most new rollups.

Unlike Arbitrum and Optimism, Base does not have its own token. Sequencer fees flow back to Coinbase, with a percentage shared with the Optimism Collective under the Superchain agreement. The no-token approach has drawn both praise (for reducing speculative noise) and criticism (for lacking a decentralized governance vote).

The chain has been popular among several categories:

- Memecoin and social tokens

- Consumer NFT projects

- Onchain payments and stablecoin flows (USDC circulation on Base crossed $5 billion in early 2026)

Head-to-Head Comparison: L2 fees, TVS, and Ecosystem

The simplest way to compare L2 fees, security, and ecosystem depth is in a side-by-side view, note that data is a subject to change.

| Metric | Arbitrum | Optimism | Base |

| TVS (early 2026) | ~$15B | ~$1.5B | ~$12B |

| L2 DeFi share | ~38% | ~3.7% | ~30% |

| Avg. transaction fee | ~$0.005–$0.30 | ~$0.05–$0.50 | ~$0.01–$0.30 |

| Block time | ~0.25s | 2s | 2s |

| Rollup type | Optimistic (multi-round fraud-proof) | Optimistic (multi-round) | Proprietary unified stack (ex-Optimistic multi-round) |

| Stage classification | Stage 1 | Stage 1 | Stage 1 |

| Native token | ARB | OP | None |

| Sequencer | Offchain Labs (centralized) | Optimism (centralized) | Coinbase (centralized) |

| Flagship integration | Robinhood Chain | Ink, Unichain, Soneium | Coinbase |

| Ecosystem position | DeFi depth, institutional RWAs | Modular Superchain | Consumer apps, retail funnel |

The L2 Consolidation

The DeFi TVL 2026 picture is sharply concentrated. 21Shares’ December 2025 “State of Crypto” report flagged that more than 50 rollups compete for users, but only three (Base, Arbitrum, Optimism) handle close to 90% of all L2 transactions.

The data illustrate a power-law distribution. Together, Base and Arbitrum represent over 68% of the total value secured across all L2s. Smaller chains have struggled:

- Kinto has shut down

- Loopring closed its wallet

- Blast TVS collapsed by roughly 97% from the peak

Even blue-chip protocols like Aave and Synthetix scaled back deployments on weaker chains, citing thin liquidity and limited rewards for liquidity providers.

The thesis is straightforward. L2 winners did not win on technical superiority. They won on distribution: Coinbase users for Base, institutional rails for Arbitrum, and the OP Stack federation for Optimism. For a broader L2 context, specifically on sidechains see how Polygon is repositioning around POL and zkEVM in our overview of Polygon staking.

What This Means for ETH Stakers

L2 activity flows back to Ethereum in two ways. First, every L2 transaction settles to the mainnet, and rollups pay Ethereum for blob data through EIP-4844.

Second, deeper L2 ecosystems pull more ETH onto rollups as gas, collateral, and liquidity, which potentially strengthens the broader staking thesis.

According to Ethereum Foundation, For ETH stakers, healthier L2s deliver several benefits:

- Ethereum L1 remains the settlement and liquidity hub. Every L2 transaction ultimately settles on L1, meaning more L2 activity directly translates to more demand for Ethereum‘s base layer security, which stakers provide.

- ETH‘s multi-role advantage is structural. ETH functions simultaneously as a gas and application asset across the entire L1+L2 stack, making it the native unit of account for every transaction settled on Ethereum.

- L2 growth extends Ethereum‘s network effects. As L2s onboard new users and developers, they feed back into Ethereum‘s validator economy through bridge inflows, blob fees, and settlement demand, all of which benefit stakers.

- A stronger L1 is a prerequisite for a healthy L2 ecosystem. The EF frames L1 scaling (while preserving decentralization) as the foundation.

- Stage 2 and native rollups deepen L1 dependency. As more L2s push toward full trustlessness and native rollup status, their security reliance on L1 grows, creating more durable and structural demand for ETH staking.

- Blob market headroom reflects room for the network to absorb L2 growth. Blobs are only ~30% full today per the EF. As L2 adoption scales, blob demand and associated fees to validators may be expected to increase alongside settlement activity.

If you want to help secure this base layer, you can stake ETH directly at the protocol level with Everstake.

The bottom line is that a healthy L2 stack may increase the long-term staking rewards, as validator demand is directly tied to settlement activity.

FAQ

Is Base bigger than Arbitrum?

It depends on the metric. Base is larger by daily transactions and active addresses. Arbitrum is larger by total stablecoin balances and institutional deposits, with TVS hovering around $15.5 billion in early 2026.

Which L2 has the lowest fees?

Average L2 fees are very close across the top three. Arbitrum typically posts the lowest median fee (around $0.005 for simple transactions post-Dencun), with Base and Optimism sitting just above. Spikes happen during DEX volume surges or NFT mints, especially on Base.

Can you stake on L2s?

You cannot stake ETH directly to validate Ethereum from inside an L2.

What is the Robinhood Arbitrum chain?

Robinhood Chain is an L2 built on Arbitrum Orbit, designed for tokenized real-world assets like stocks and ETFs. The testnet went live on February 10, 2026, and processed 4 million transactions during its first week. Mainnet is targeted for later in 2026.

What is Kraken’s Ink L2?

Ink is Kraken’s L2, built on the OP Stack and part of the Optimism Superchain. It launched in December 2024 with one-second block times and sub-cent fees.

Will smaller L2s survive 2026?

The L2 market is highly concentrated. According to 21Shares’ December 2025 data, Base, Arbitrum, and Optimism together handle close to 90% of all L2 transactions. Smaller chains without distribution advantages or ecosystem alignment have struggled in 2025. Whether that trend continues depends on technical development, liquidity incentives, and broader market conditions.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, legal, or tax advice. Nothing here is an endorsement or recommendation to buy, sell, hold, or stake any digital asset, or to use any platform or service mentioned. Mention of third parties does not imply affiliation or endorsement.

Digital assets and staking carry significant risks, including volatility, regulatory uncertainty, and total loss of capital. Data referenced reflects publicly available sources as of the date of publication and may change. Readers should conduct their own research and consult qualified professionals before making any decisions.

Share with your network