ethereum

Ethereum Supply, Issuance and Staking Debate Overview

More than one-third of all ETH is now staked, a threshold the network has never crossed, driven by institutional adoption and liquid staking tokens. Researchers are split between reforming the reward curve, preserving the current model, and addressing Ethereum’s L1 value capture instead.

MAY 28, 2026

Last updated MAY 28, 2026 · V1

TL;DR:

- As of April 2026, over 1/3 of all ETH supply is staked in Ethereum‘s consensus layer — a threshold the network has never previously crossed.

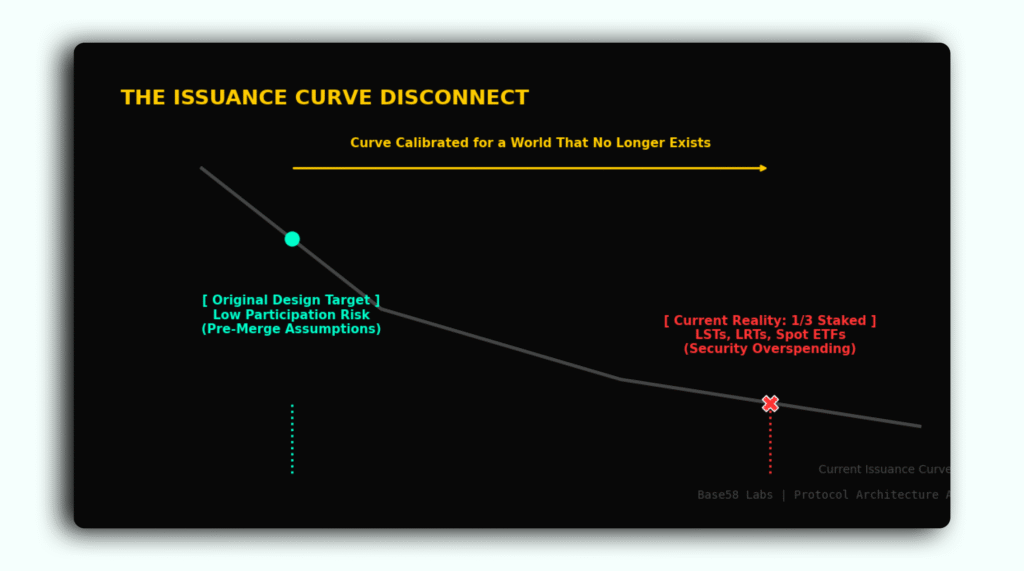

- The staking ratio is rising because the current issuance curve was designed for a 20–25% staking target that liquid staking tokens (LSTs) and institutional adoption have made structurally obsolete.

- Net ETH issuance runs at approximately 0.7–0.8% annually, and absent a change to the reward curve, protocol mechanics will push the ratio toward 100% over time.

- No issuance change is expected before Glamsterdam, the hard fork after Fusaka.

- This article is a reading into the existing discussion, and does not represent the company’s official position

Why the Question Is Triggered Again

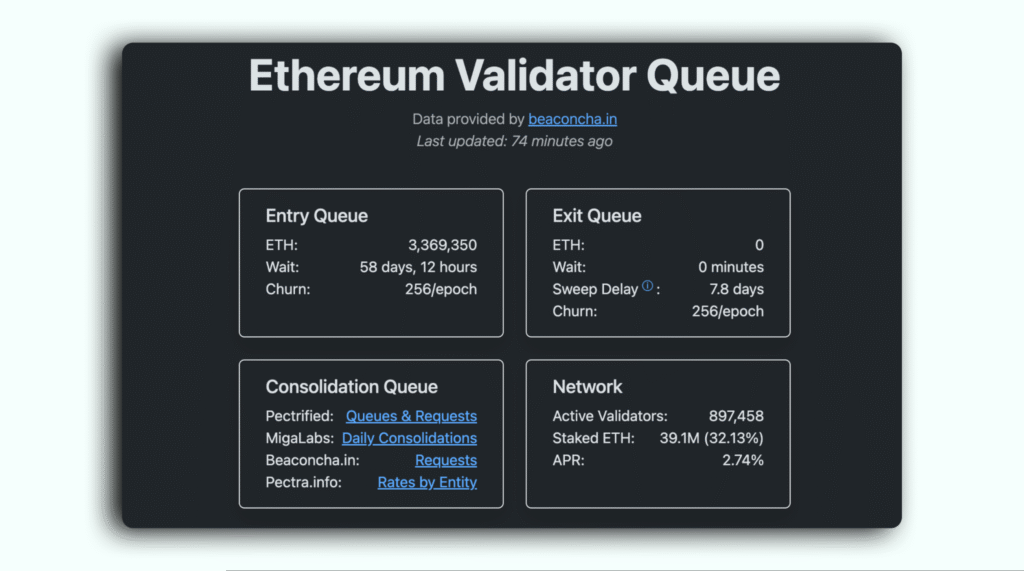

The debate over Ethereum‘s staking issuance is not new, but in April 2026 it moved from background discussion to the front of Ethereum‘s governance agenda. The discussion was ignited because the share of ETH staked in the consensus layer has crossed the 1/3 threshold for the first time and continues to grow.

The entry queue has consistently reached around 50-60 days.

As researcher Pintail noted in an April 2026 analysis, the current staking ratio is the direct product of an issuance curve designed before liquid staking existed. Liquid staking has drastically changed the economics of staking.

Several forces converged to bring us here. The SEC‘s May 2025 decision to clarify that staking services generally fall outside its enforcement jurisdiction removed a legal barrier for US financial institutions.

ETF providers and Digital Asset Treasuries (DATs) began committing ETH to the consensus layer at scale. Most visibly BitMine, which held approximately 5.39 million ETH in treasury with ~4.7–4.8 million ETH already staked by mid-May 2026, and announced plans to stake virtually all remaining holdings.Though its contribution will likely slow as it approaches full deployment of its remaining unstaked ETH.

It is worth mentioning that not all DATs are adding to their positions:

Meanwhile, liquid staking tokens (LSTs) had already practically removed the illiquidity barrier that once made staking less attractive relative to holding raw ETH.

The Mechanics: How Growing Stake Affects Issuance

Ethereum’s reward curve has a balancing mechanism: the more ETH gets staked, the lower the staking rewards for each individual validator.

As participation grows, the protocol automatically reduces staking rewards issuance, designed to discourage the staking ratio from climbing too high.

At the 20–25% staking ratio the original designers targeted, nominal APR is around 4%. At today’s 30%+, it has compressed to roughly 2.8%. This model was created before the LSTs, when the network participants received staking rewards also partly for the inconvenience of their ETH being illiquid.

Now the inconvenience is removed via LST. This model might be outdated in terms of modern realities of Ethereum. When stakers receive a reward-bearing token they can freely deploy in DeFi (as collateral, in lending, or as restaking collateral), the opportunity cost of locking ETH is effectively eliminated.

The protocol responds by lowering staking rewards, but stakers recover the difference by putting their LSTs to work in DeFi.

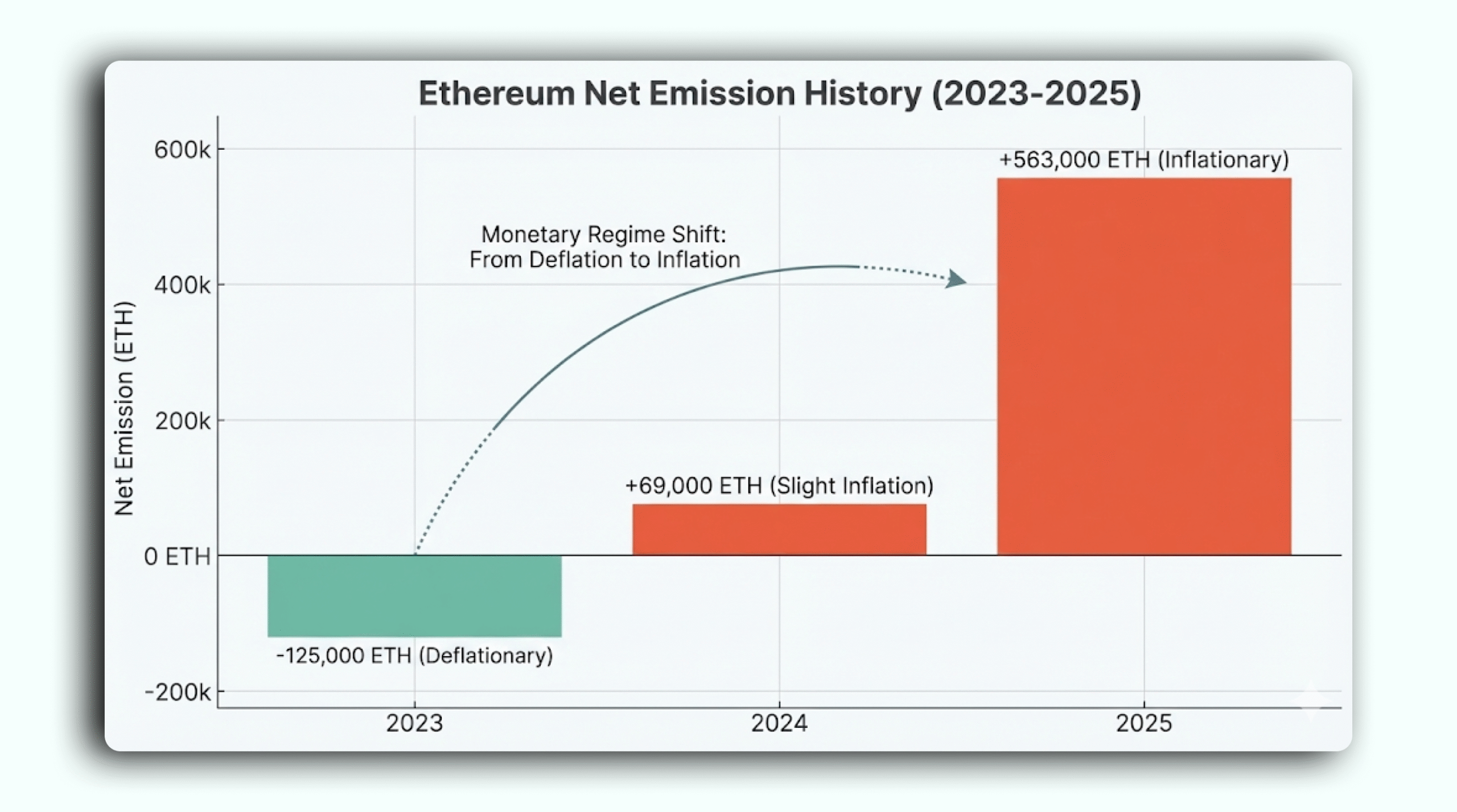

As a result, gross issuance rises, as well as the staking ratio. If token burn from base fees does not keep pace, Ethereum moves from net deflationary to net inflationary on supply.

Before L2s took off, high L1 fees were burning enough ETH to make the network deflationary, supply was shrinking. Now burn has dropped and issuance is rising.

Net issuance currently runs at approximately 0.7–0.8% annually.

Everstake flagged this before in the 2025 Annual Protocol Analysis: Ethereum has moved from a “deflation through high costs” model to “low inflation for mass adoption.” This is the price the protocol pays for the sake of scalability. The main question is if the current trajectory stays within acceptable bounds.

Overstaking, Not Just High Staking

Past a certain threshold, additional stake doesn’t tangibly influence network security, while continuing to impose dilution costs on non-stakers.

The marginal unit of staked ETH past 30% does not meaningfully reduce the cost of a 51% attack but rather increases gross issuance.

High staking ratios potentially create another type of risk. If a small number of providers come to dominate (a plausible outcome given network effects in staking infrastructure) the slashing mechanism that enforces Ethereum‘s economic security may become effectively unusable.

A provider controlling a sufficiently large share of stake becomes, in practice, too large to slash without systemic collateral damage. At that point, the security model becomes more fragile.

There is also a tipping point that receives less attention: the level at which solo stakers face negative real reward. At high staking ratios, nominal APR might be substantially offset by dilution.

Solo stakers in most jurisdictions may also pay income tax on nominal rewards in the year received. The combination means solo staker effective reward (dilution-adjusted, after tax) can turn negative well before the staking ratio reaches 100%.

Three Schools of Thought

The debate has crystallized around 3 distinct positions.

Reform the issuance curve

Researchers including Ansgar Dietrichs, Caspar Schwarz-Schilling, and Anders Elowsson have argued for adjusting the reward curve to target a specific staking ratio rather than allowing unbounded growth.

Proposals range from a simple scalar cut (reducing BASE_REWARD_FACTOR from 64 to 32) to more structurally durable tempered formulas that compress rewards more aggressively beyond the originally-intended 20–25% band.

Grayscale has since offered the asset-management version of the same argument: lower issuance reduces supply growth, increases ETH scarcity, analogous to lower production for a physical commodity.

Preserve the existing model

LST operators and portions of the DeFi ecosystem have pushed back against the proposed staking issuance changes, arguing that LSTs now play a significant role in Ethereum’s on-chain finance stack. The reaction below illustrates concern from the Lido community side:

A material reward cut reduces staking incentives, shrinks LST supply, and compresses the collateral base that lending markets, restaking protocols, and curated vaults depend on.

The counter-argument to “DeFi existed before LSTs” is that today’s DeFi is structurally different and the feedback loops between LST reward and protocol TVL run much deeper than they did in 2020.

The problem is value capture, not issuance

A third camp, increasingly prominent in spring 2026 discussions, argues that high staking ratios are a symptom rather than a cause. The real issue is that Ethereum‘s L1 is capturing less economic value as:

- activity migrates to L2s

- base fees remain structurally low

- blob pricing has been intentionally kept cheap to support scaling.

In this framing, tinkering with the reward curve treats the visible metric without addressing what drives it.

The Case for Nuance

Everstake operates staking infrastructure across Ethereum and discloses this interest directly. The views below reflect Everstake‘s reading of publicly available research, discussions and on-chain data as of May 2026, and do not represent the company’s official position.

A rising staking ratio is NOT a signal for protocol failure

In uncertain or range-bound markets, staking functions as a behavioral anchor: it gives ETH holders a way to maintain exposure to the asset while participating in protocol reward generation, rather than leaving ETH entirely idle.

The narrative that LSTs caused the overstaking problem deserves scrutiny

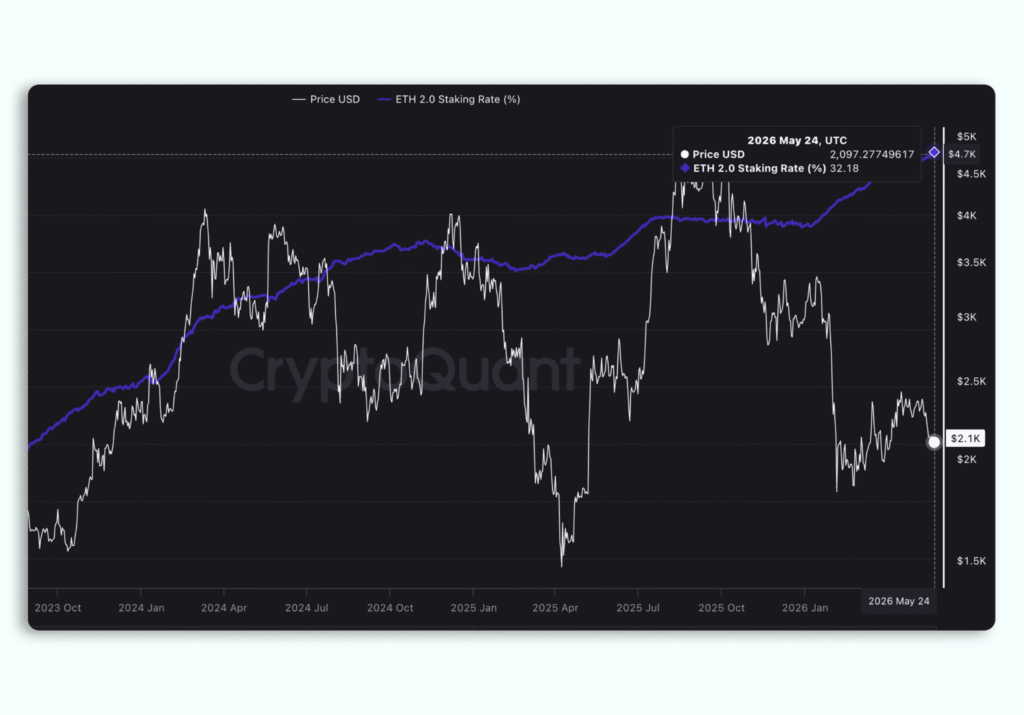

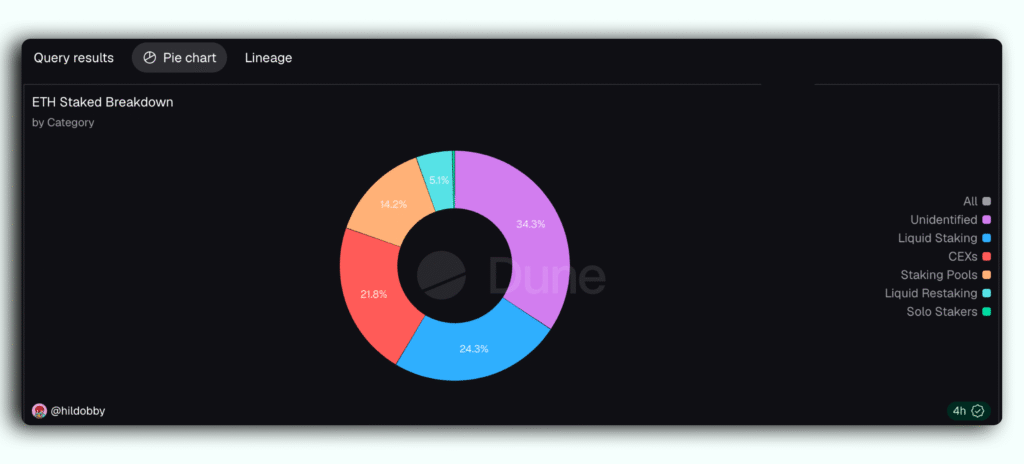

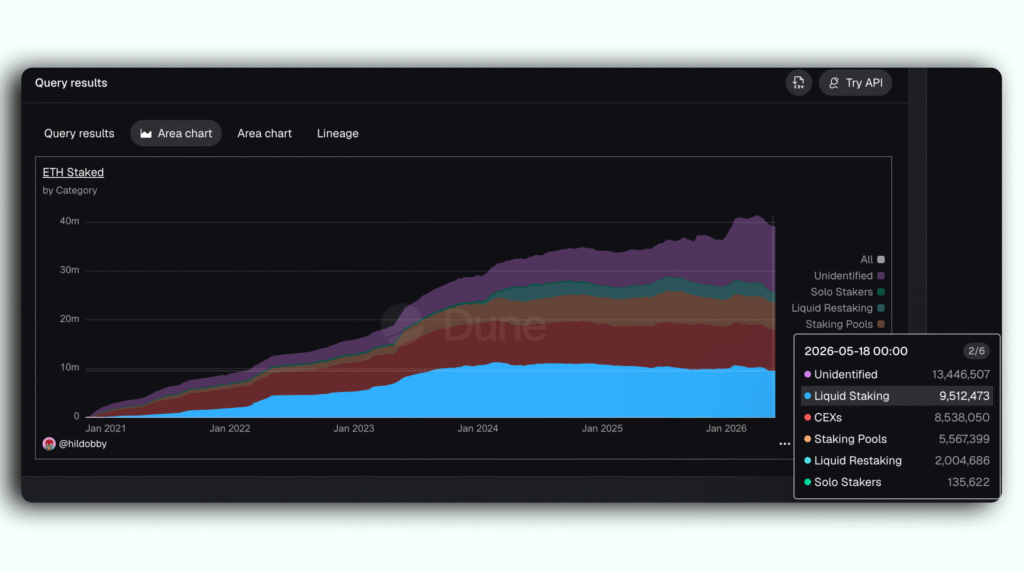

LST market share of total staked ETH has declined from approximately 37.8% at end-2023 to around 24.3% as of May 2026.

Even as the absolute amount of ETH staked has remained roughly stable near 9–11 million ETH.

The growth in total staked ETH has outpaced LST growth, suggesting LSTs lowered the technical barrier to entry while the incremental demand seems to be coming from elsewhere:

- native stakers,

- institutional ETF exposure,

- DAT treasury strategies.

For most ETH holders, the staking rewards may be secondary to the price direction of the asset

The Grayscale point about ETH price volatility is also worth foregrounding: annualized volatility of ~60% equates to roughly 1 day of price movement per year of staking APR.

This does not make issuance irrelevant, since 0.7–0.8% annual net supply growth is not zero, and it compounds. It does imply the stakes of the issuance debate are often overstated in the short term.

The value-capture argument might be the most analytically useful long-term frame

Strengthening L1 fee capture, improving blob pricing dynamics, and growing the economic activity that generates burn are interventions that address the underlying utility driver rather than adjusting a downstream parameter.

When Ethereum’s L1 processes more activity, higher fees burn more ETH naturally offsetting issuance the way it did during the 2021-2023 boom. That deflationary pressure is what made the growing staking ratio irrelevant back then.

But rebuilding that fee burn takes time, and the staking ratio is rising now, so fixing Ethereum’s value capture and adjusting the reward curve need to move forward at the same time.

Potential changes to validator activation and exit throughput could take some pressure off the staking ratio

One worthy near-term development is EIP-8061, currently in devnet testing for the Glamsterdam upgrade. It aims to increase validator activation and exit throughput, potentially cutting the current 55–65 day entry queue by more than 2/3. Faster entry and exit reduces one structural incentive to stay staked past the point of conviction: the friction cost of a long queue.

If getting out becomes easier, the staking decision becomes more continuous and market-responsive, which may naturally moderate ratio growth at the margin.

What Comes Next

No issuance change is imminent.

- Pectra deferred the question.

- Fusaka is focused on PeerDAS and data scaling.

- Glamsterdam is the earliest realistic window for a curve-modifying EIP.

Even that depends on whether researchers, client teams, and the broader community can converge on a specific proposal. Current ecosystem discussions suggested the core developer community is in no rush.

What has changed is just the visibility of the debate.

LST operators, Ethereum Foundation researchers, and asset managers are now making their arguments openly about BASE_REWARD_FACTOR, curve shapes, and staking ratio targets. Questions that once lived in research forums are now part of the active protocol roadmap conversation, which is great for transparency.

Any issuance reform will play out differently depending on what else changes around it: how Glamsterdam‘s upgrades reshape validator economics and how future scaling decisions influence L1 fee burn. The net effect on the ecosystem depends on all of these and more factors moving together, not on the issuance change in isolation.

Disclaimer

This article is published by Everstake for informational purposes only. Nothing in this article constitutes financial, legal, investment, or tax advice, and it should not be relied upon as such. The analysis, opinions, and conclusions expressed here reflect Everstake‘s reading of publicly available research, on-chain data, and ecosystem discussions as of May 2026 they do not represent Everstake‘s official position, and reasonable analysts may disagree with the interpretations presented. Readers should conduct their own due diligence and consult qualified professional advisors before making any decisions in connection with the topics discussed.

Share with your network