Aptos

sui

Sui vs. Aptos: Comparing Move-Based Blockchain Staking Rewards (2026)

Technical deep-dive comparing Sui and Aptos staking yields in 2026. Storage Fund vs Inflation Model.

MAR 17, 2026

Last updated MAR 20, 2026 · V1

Sui and Aptos are the two leading Move-based L1 blockchains, yet their staking economics work in fundamentally different ways. For delegators and institutional allocators evaluating the Sui vs Aptos staking decision, those differences matter more in 2026 than at any prior point in each network’s short history.

Introduction to Sui and Aptos’ Current Affairs

In February 2026, the Aptos Foundation proposed a sweeping tokenomics overhaul: a hard supply cap of 2.1 billion APT, a cut in the staking APR from 5.19% down to 2.6%, a tenfold increase in gas fees, full burning of base fees, and the permanent lock of 210 million APT. The goal was a shift from pure inflation-driven rewards toward a deflationary model. At the same time, Sui’s Storage Fund mechanism continued to deliver approximately 7% staking rewards, both from newly minted tokens and a distinct rewards layer funded by on-chain storage fees.

It, therefore, stands to reason to run a comparison of reward mechanics, tokenomics architecture, and long-term staking sustainability across both Move-based networks. Whether you are a professional delegator, a validator operator, or an institution evaluating digital asset rewards strategies, the distinctions laid out here are the ones that will shape real rewards in 2026 and possibly beyond.

Everstake operates validators on both Sui and Aptos, giving us direct visibility into reward mechanics, epoch economics, and the performance of real rewards across both Move-based networks. That operational perspective informs every section of this comparison.

Move-Based Blockchains: Shared DNA, Different Design

Sui and Aptos share a common origin. Both were founded by engineers who previously worked on Meta’s Diem blockchain project, and both adopted Move as their smart contract language. Both target high-throughput, low-latency execution as core design objectives. That shared foundation is where the similarities become most apparent, and where the divergences begin to matter for staking economics.

Sui: Object-Centric Execution

Sui implements a variant of Move in which digital assets are first-class objects with globally unique identifiers. This object-centric model means that transactions operating on independent objects carry no shared-state conflicts, as the protocol can execute them in parallel without requiring a global ordering step. Sui’s consensus layer, Mysticeti (an evolution of the earlier Narwhal and Bullshark protocols), is designed around a directed acyclic graph structure that exploits this independence directly.

The practical consequence for staking is significant: because object ownership is explicit, Sui’s storage model charges a one-time fee per object rather than a recurring per-transaction cost. Those fees accumulate in the Storage Fund, which becomes a separate and permanent source of validator rewards.

Aptos: Account-Based Execution

Aptos uses an account-based data model closer in spirit to Ethereum: state lives in accounts, and transactions modify account balances or module state. To achieve parallel execution on top of this model, Aptos leverages Block-STM to manage high-throughput loads, which reduces the risk of transaction failure during peak volatility by using optimistic concurrency with conflict detection and rollback rather than requiring sequential ordering.

AptosBFT consensus delivers sub-50ms block finality and has maintained 99.99% uptime since mainnet launch. These are genuine operational strengths, but the account model means Aptos has no structural equivalent to Sui’s Storage Fund, and its validator rewards therefore remain dependent on the interplay of inflation, fee burns, and staking participation rates.

Why the Data Model Drives Rewards Structure

The choice between object-based and account-based architectures is crucial. On Sui, object-level storage fees create a compounding fund whose staking rewards grow in proportion to network data demand. On Aptos, validator rewards flow from inflation and from transaction fees that are now burned rather than distributed. The MoveVM staking comparison ultimately reduces to this single structural difference: one network monetizes storage as a long-term rewards source, while the other bets that deflation via burns will compensate for reduced inflation rewards.

Sui Staking: The Storage Fund Model

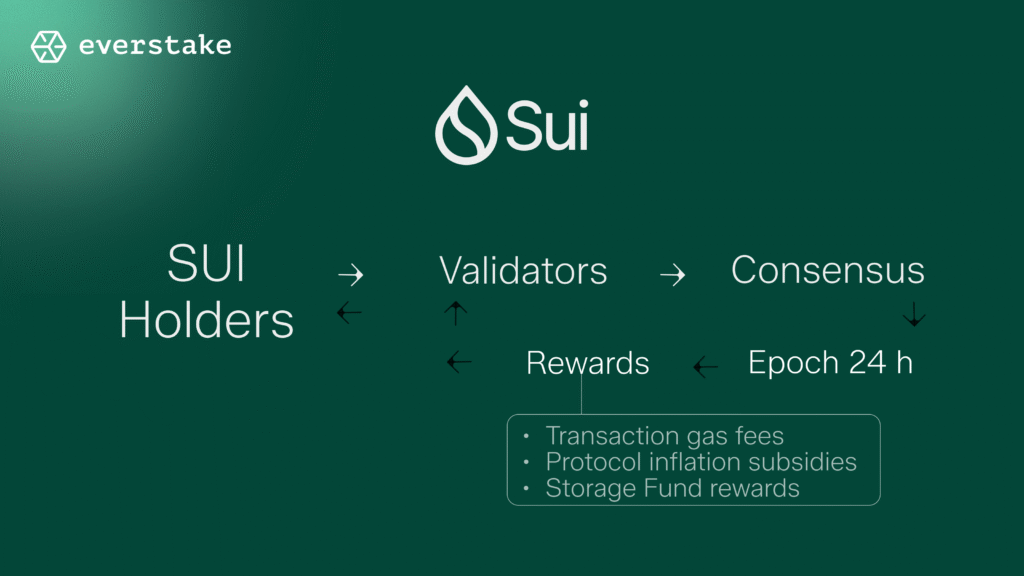

Sui uses a delegated proof-of-stake model in which SUI holders assign their tokens to validator nodes, which in turn participate in consensus and earn rewards on behalf of delegators. Each epoch lasts 24 hours, and rewards are calculated and distributed at each epoch boundary. The minimum stake is 1 SUI, and unstaking is available at every epoch transition, i.e., there is no multi-week lockup.

Three Streams of Incentives

What distinguishes Sui’s staking APR from most alternatives is the composition of its rewards. Sui validators draw from three separate rewards streams:

- Computation gas fees paid by users for transaction processing

- Stake reward subsidies drawn from protocol inflation

- Storage Fund distributions, i.e., returns generated by staking the accumulated storage fees

This three-stream structure means Sui staking is not purely inflation-dependent. Even if protocol subsidies were reduced significantly, the Storage Fund would continue to generate returns proportional to the amount of data stored on-chain.

How the Storage Fund Works

Every transaction that creates new on-chain objects pays a one-time storage fee. Those fees do not go to validators directly, but instead accumulate in the Storage Fund, a protocol-level reserve that is itself staked alongside user stake. The returns generated by the fund’s staking position compensate validators for the ongoing cost of storing data indefinitely. When users delete objects and free storage, they receive a rebate, which incentivizes data hygiene without removing the underlying economic logic.

Critically, the Storage Fund never distributes its principal. Only the returns on capital flow out as rewards. This arrangement creates a structurally growing reserve: as the network stores more data, the fund grows; as it grows, it generates more staking returns, which increase the reward baseline for all validators. The Sui storage fund staking mechanism is, in effect, a rewards floor tied to adoption rather than to a monetary policy dial.

Current Rewards and Participation Dynamics

In early 2026, Sui validators were producing approximately 7% nominal APR, though this figure varies by validator commission and by the overall staking participation rate. With 65–75% of circulating SUI supply staked, real rewards sit slightly below zero when adjusted for token inflation, which is a common pattern in high-participation PoS networks. Higher staking participation compresses nominal rewards because the same reward pool is distributed across a larger staked base.

Two institutional signals in February 2026 are worth noting: the Canary SUIS ETF, listed on NASDAQ (with Everstake participation), and the Grayscale GSUI ETF, listed on NYSE Arca, both of which incorporate staking rewards into their net asset value calculations. ETF issuers conduct rigorous due diligence on rewards sustainability before structuring a product, and thus it stands to reason to assume that the presence of two staking ETFs on Sui and none on Aptos does, in fact, reflect an implicit institutional judgment about which rewards profile is more predictable.

Everstake on Sui Infrastructure

Everstake optimizes Sui validator operations around epoch-level predictability. Because the Storage Fund contribution to rewards is a function of accumulated on-chain storage rather than a discrete governance decision, rewards modeling becomes more tractable for delegators with structured reporting requirements.

Everstake’s monitoring infrastructure tracks epoch reward variance, commission structures, and Storage Fund growth metrics to provide institutional-grade reporting on Sui staking performance.

Aptos Staking: From Inflation to Deflationary Transition

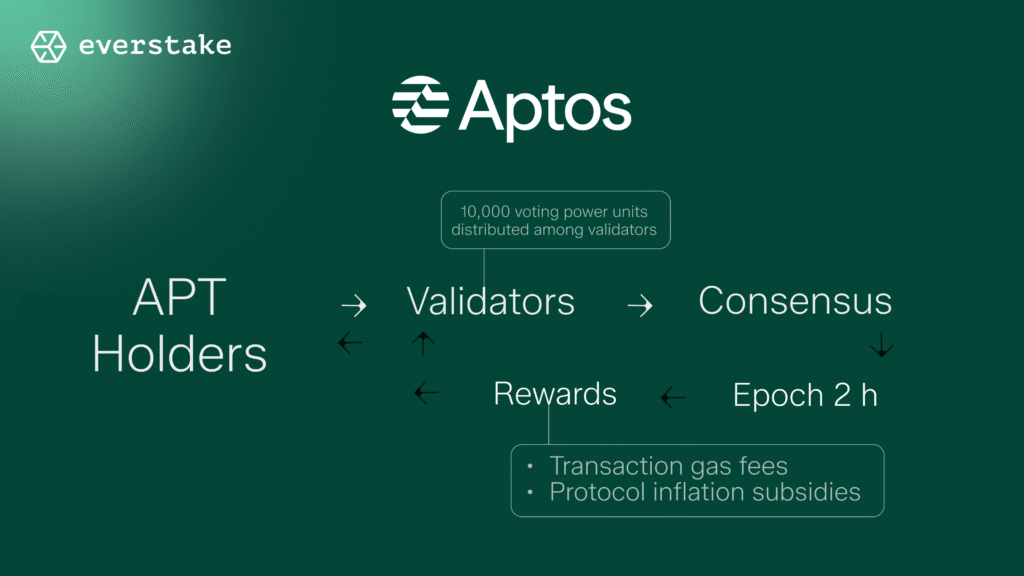

Aptos staking also uses a delegated proof-of-stake architecture. Still, its validator structure differs from Sui’s in one important respect: the Aptos network distributes 10,000 total voting power units across all active validators, with a cap of 1,000 units per individual validator. This concentration cap limits any single operator’s network dominance, though it also means that smaller validators may face marginal economics as the staking reward rate falls.

APT holders delegate to validators and receive inflation-based staking rewards, as well as a share of transaction fees. Epochs on Aptos are approximately 2 hours long, producing roughly 7,200 epoch transitions per year, which is objectively a much finer reward granularity than Sui’s daily cycle.

The 2026 Tokenomics Overhaul

On February 18, 2026, the Aptos Foundation proposed the most substantive change to Aptos tokenomics since mainnet launch. The key elements of the overhaul:

- A hard supply cap of 2.1 billion APT, ending Aptos’ previously open-ended inflationary schedule

- Staking annual returns cut from 5.19% to 2.6%, roughly halving the annual reward rate for delegators

- Gas fees increased tenfold (base transaction cost remains near $0.00014, keeping Aptos practically free for users, while generating more total fee volume for burning)

The overhaul also included permanently locking 210 million APT staked by the Aptos Foundation, eliminating discretionary grants in favor of milestone-based disbursements, and introducing a potential token buyback program.

Aptos tokenomics deflationary 2026 logic rests on the burn mechanism. If Decibel DEX volume and broader application activity generate enough fee throughput, burned tokens will exceed newly minted staking rewards, causing the net circulating supply to decline. As of the proposal date, however, on-chain fees were running at approximately $680 per day. In principle, this figure would need to scale dramatically for the burn rate to outpace emissions.

Risk Factors in the Transition

The Aptos staking rewards 2026 cut raises a genuine concern for validator economics. At 2.6% APR, validators operating with high infrastructure costs may find the margin too thin to sustain professional-grade operations. If validators exit the active set, network security declines, which can trigger a negative feedback loop: fewer validators reduce confidence, reducing delegator participation, further compressing fee revenue. APT’s price declined approximately 87% from its February 2025 peak despite the overhaul announcement, adding further pressure on validators whose costs are denominated in fiat currencies.

One significant milestone on the 2026 timeline would be in October 2026, when the conclusion of the four-year investor unlock cycle for early Aptos backers is expected. This event would reduce annual new supply unlocks by approximately 60%, removing a persistent source of structural selling pressure that has weighed on APT since mainnet launch.

Everstake on Aptos Infrastructure

Everstake operates within Aptos’ voting power structure, aiming for stable, long-horizon validator participation. The shift to milestone-based Foundation grants and the 210M APT permanent lock introduces more predictable Foundation behavior. Still, it also means that network growth must now come from organic usage rather than treasury-funded initiatives. Everstake’s Aptos infrastructure team actively models delegator behavior under the new 2.6% APR regime to anticipate rebalancing flows across the validator set.

Sui vs. Aptos: Side-by-Side Comparison

| Category | Sui | Aptos |

| Consensus | Mysticeti (DAG-based) | AptosBFT |

| Data Model | Object-centric | Account-based |

| Parallel Execution | Native (object independence) | Block-STM (optimistic) |

| Move Variant | Sui Move | Aptos Move |

| Epoch Length | 24 hours | 2 hours (~7,200 epochs/year) |

| Min Stake | 1 SUI | 11 APT (validator min: 1M APT) |

| Staking APR (2026) | ~7% nominal | ~2.6% (post-overhaul) |

| Reward Sources | Gas + subsidies + Storage Fund | Inflation + transaction fees |

| Inflation Model | Decreasing subsidy + Storage Fund | Capped at 2.1B APT, 100% burn |

| Tokenomics 2026 | Storage Fund growing with usage | Deflationary if burns > emissions |

| Staking Participation | ~65–75% circulating supply | Not publicly disclosed |

| Staking ETFs | Canary SUIS, Grayscale GSUI | None (as of Feb 2026) |

| Validator Commission | Variable by operator | Variable: 10,000 voting units total |

| Unstaking Period | Epoch boundary (daily) | ~30-day lockup |

| Storage Fee Mechanism | One-time fee -> Storage Fund | N/A (standard gas model) |

Rewards Sustainability: Storage Fund vs. Deflationary Burns

The central question for any long-term delegator is hardly about the rewards in the moment, but about what structural forces will sustain or erode them over the next two to four years. Sui and Aptos offer fundamentally different answers.

Sui’s Structural Advantage

Sui’s object-based vs account-based blockchain architecture creates a rewards layer that scales with actual network utilization. As more applications store data on Sui (whether DeFi positions, gaming assets, or tokenized real-world assets), the Storage Fund grows. A larger fund generates more staking returns, which partially offsets the natural rewards compression that comes with rising staking participation. This feedback loop is slow-moving and structural rather than dependent on any governance vote or monetary policy change.

The practical implication here is that Sui staking APR has a floor that rises with adoption, even if protocol subsidies continue to taper. This issue is a materially different risk profile than a network whose rewards depend entirely on the balance between new issuance and fee burns.

Aptos’ Aspirational Model

The Aptos deflationary thesis is credible in theory, but requires a significant step-change in transaction volume to operate as designed. Current daily fee revenue of approximately $680 would need to increase by orders of magnitude before burns meaningfully offset the approximately 2.6% annual emissions on a supply approaching 2.1 billion APT. The Decibel DEX launch and continued DeFi ecosystem expansion are catalysts that could drive volume, but they are not yet proven at the scale the model requires.

The October 2026 investor unlock conclusion is likely to remove the largest external supply pressure. If fee volume scales alongside the reduction in new supply unlocks, Aptos could achieve the deflationary crossover its tokenomics are designed for. Until then, the model is a well-designed aspiration running ahead of the fee infrastructure needed to validate it.

Institutional Signal: ETFs as Rewards Endorsement

The move to blockchain staking, as compared in early 2026, adds a data point that institutional allocators should weigh: Sui has two staking ETFs, while Aptos has none. ETF issuers do not structure reward-inclusive products without extensive analysis of reward sustainability, custody arrangements, and regulatory treatment. The Canary SUIS and Grayscale GSUI listings represent a de facto institutional endorsement of Sui’s rewards profile as sufficiently predictable to underwrite in a regulated fund structure.

That does not mean Aptos staking is without merit: the deflationary overhaul is a structurally sensible response to inflationary fatigue across the PoS ecosystem. But the absence of an equivalent ETF product on Aptos reflects a gap in institutional confidence that the new model has yet to close.

Frequently Asked Questions

What is Sui’s Storage Fund?

The Storage Fund is a protocol-level reserve that accumulates one-time storage fees paid by users when they create on-chain objects. The fund is staked alongside user delegations, and the returns on that staking position compensate validators for the perpetual cost of storing data. The principal of the fund is never distributed, which makes it a compounding, usage-driven addition to the standard inflation-based reward structure.

How do Aptos staking rewards change in 2026?

Aptos staking rewards in 2026 are set to fall from 5.19% APR to approximately 2.6% APR as part of the February 2026 tokenomics overhaul. The reduction accompanies a hard supply cap of 2.1 billion APT, a tenfold increase in gas fees, full burning of base fees, and the permanent lock of 210 million APT by the Foundation. The intent is to transition from inflation-funded rewards toward a burn-driven deflationary model.

Which has higher staking rewards: Sui or Aptos?

As of early 2026, Sui offers approximately 7% nominal staking APR compared to Aptos’ 2.6% post-overhaul APR. Sui’s rewards advantage is meaningful in absolute terms. However, the rewards on both networks depend on token price performance, staking participation rates, and, specifically on Sui, the Storage Fund’s growth rate.

What is the difference between Sui Move and Aptos Move?

Both are variants of the Move programming language, but they diverge in their data models and execution semantics. Sui Move treats assets as first-class objects with unique global identifiers, enabling native parallel execution of independent transactions. Aptos Move uses an account-based model closer to Ethereum’s architecture, with Block-STM providing parallel execution through optimistic concurrency and conflict resolution rather than through inherent object independence.

Are there Sui or Aptos staking ETFs?

As of February 2026, two Sui staking ETFs are operating: the Canary SUIS ETF on NASDAQ and the Grayscale GSUI ETF on NYSE Arca, both of which incorporate staking rewards into their NAV calculations. No equivalent staking ETF product exists for Aptos at this time.

Is Aptos becoming deflationary?

The February 2026 tokenomics overhaul creates the conditions for Aptos to become deflationary, but only if transaction fee volume (primarily through burning) exceeds new token emissions. Current fee revenue of approximately $680 per day falls well short of the threshold required. The model is architecturally sound. Whether it operates as intended depends on the growth of Aptos application usage, particularly Decibel DEX and other high-volume protocols.

Does Everstake validate on both Sui and Aptos?

Yes. Everstake operates validator infrastructure on both Sui and Aptos, providing direct operational visibility into epoch economics, reward variance, and real rewards performance on each network. This dual-network presence informs Everstake’s technical analysis and allows delegators to access institutional-grade staking on both Move-based chains through a single operator.

Which Move blockchain is better for long-term staking?

The choice depends on risk profile and time horizon. Sui’s Storage Fund mechanism offers a more structurally stable rewards floor, with reward sustainability tied to data storage adoption rather than governance decisions. Aptos’ deflationary model offers upside if fee volume scales as projected, with the October 2026 investor unlock conclusion removing a major structural headwind. Institutional allocators with lower tolerance for reward variability may currently favor Sui’s more predictable reward architecture. Delegators with higher risk appetite may find Aptos’ asymmetric tokenomics compelling at the 2.6% base rate.

Disclaimer

The information provided is not intended for recipients residing in the United Kingdom.

Share with your network