ethereum

Institutional

Ethereum Staking ETFs Explained: How They Work and What They Mean for Institutions

Ethereum staking ETFs combine ETH price exposure with network staking rewards through products like Grayscale’s ETHE and BlackRock’s ETHB. A March 2026 SEC/CFTC joint release classifying staking rewards as non-securities cleared the regulatory path, with five more issuers awaiting approval and Solana staking ETFs offering an alternative.

APR 20, 2026

Last updated JUL 10, 2026 · V1

TL;DR

- An Ethereum staking ETF holds ETH and stakes a portion of it on the network, passing staking rewards to shareholders as a periodic distribution, unlike a spot ETF, which only tracks price.

- Two U.S. Ethereum staking ETFs are live as of April 2026: Grayscale’s ETHE (since October 2025) and BlackRock’s ETHB (since March 2026), with five more issuers awaiting approval.

- Gross staking rewards on Ethereum currently range from 3.1% to 3.3% annually. After fund fees and custody costs, net distributions to shareholders range from about 1.9% to 2.6%.

- The SEC and CFTC joint interpretive release on March 17, 2026, classified staking rewards as non-securities, removing the legal barrier that had delayed these products for over a year.

- Solana staking ETFs launched in late 2025, with products from Bitwise (BSOL) and VanEck (VSOL) offering staking rewards of approximately 6% to 7%.

What Is an Ethereum Staking ETF?

An Ethereum staking ETF is a regulated exchange-traded fund that holds Ether (ETH) and stakes a portion of those holdings on the Ethereum network to generate staking rewards, which it then distributes to shareholders.

This gives institutions and individuals access to both ETH price exposure and network-level rewards through a single, brokerage-accessible product. The concept has become central to the structure of the next wave of regulated crypto products.

Staking ETH directly requires operating or delegating to validators, managing unbonding periods (which can range from 9 to 50 days during high network activity), and navigating the complexities of custody. A staked ETH ETF abstracts all of that into a familiar wrapper.

The fund’s custodian and staking providers handle validator operations, and rewards are either added to the fund’s net asset value (NAV) or distributed as cash.

This makes the staking ETF the first class of ETF in which the fund itself plays an active role in the blockchain it tracks.

Staking ETF vs Spot ETF: Key Differences

How does a staked product differ from the spot Ethereum ETFs that have been trading since mid-2024? The differences go beyond staking rewards, touching:

- fees,

- tax treatment,

- custody mechanics,

- liquidity.

| Feature | Spot ETH ETF (e.g., ETHA) | Staking ETH ETF (e.g., ETHB, ETHE) |

| Holds crypto | Yes, holds ETH in cold storage | Yes, holds ETH with a portion staked |

| Generates staking rewards | No | Yes, typically 3.1% to 3.3% gross annually |

| Fee structure | Sponsor fee only (e.g., 0.25% for ETHA) | Sponsor fee plus staking service fee (e.g., 0.25% sponsor + 18% of staking rewards for ETHB) |

| Custody model | Qualified custodian, cold storage | Qualified custodian plus staking provider, with a portion of ETH locked in validators |

| Tax treatment | Capital gains on the sale of shares | Capital gains on the sale of shares, plus staking distributions, may be taxable as ordinary distributions (consult a tax advisor) |

| Liquidity | Full liquidity of holdings | Fund must manage reserves for redemptions due to unbonding delays |

| NAV tracking | Tracks the ETH spot price closely | Tracks the ETH spot price plus accrued staking rewards minus fees |

The core trade-off is straightforward.

- A spot ETF offers clean price exposure with no operational complexity.

- A staking ETF introduces additional moving parts but compensates holders with staking rewards.

At a 2.5% net annual reward rate, a staking ETF would accumulate roughly 12.8% more ETH than a spot ETF over 5 years, assuming constant reward rates and reinvested distributions.

Current Market: ETHA, ETHB, and the Issuer Landscape

As of April 2026, the U.S. Ethereum ETF market includes both spot-only and staking-enabled products. The two live staking products are Grayscale’s Ethereum Staking ETF and BlackRock’s iShares Staked Ethereum Trust ETF. Several more are in the regulatory pipeline.

Grayscale Ethereum Staking ETF (ETHE) was the first U.S.-listed spot crypto product to enable staking.

Key details:

- Grayscale activated staking for ETHE and its companion Grayscale Ethereum Staking Mini ETF (ticker: ETH) on October 6, 2025.

- On January 5, 2026, it renamed the fund from “Grayscale Ethereum Trust ETF” to “Grayscale Ethereum Staking ETF” to reflect the product’s core function.

- That same day, it made the first staking distribution by a U.S. Ethereum ETF: $0.083178 per share, covering rewards accrued between October 6, 2025, and December 31, 2025.

- ETHE held approximately $3.5 billion in managed tokens as of April 2026, and charges a 2.5% annual fee.

iShares Staked Ethereum Trust ETF (ETHB) launched on March 12, 2026, with $107 million in seed capital from BlackRock.

Key details:

- The fund trades on Nasdaq and stakes between 70% and 95% of its ETH holdings through Coinbase Prime.

- Shareholders receive roughly 82% of gross staking rewards, distributed monthly. The remaining 18% covers validator operations and BlackRock’s fee.

- The sponsor fee is 0.25%, with a promotional rate of 0.12% on the first $2.5 billion in assets for the initial 12 months. ETHB reached $254 million in managed tokens within its first week.

- BlackRock kept ETHA (its spot-only Ethereum Trust, holding roughly $6.9 billion in managed tokens) as a separate product for pure price exposure.

- This two-product approach mirrors how BlackRock offers accumulation and distribution versions of its equity ETF lineup.

Pending staking amendments have been filed by Fidelity, Franklin Templeton, Invesco, 21Shares, and VanEck.

These issuers are seeking to add staking to their existing spot Ethereum ETFs. The remaining amendments are expected to clear final review windows in Q2 2026.

How Staking Rewards Are Passed to ETF Users

The ETF’s qualified custodian (such as Coinbase Custody) delegates a portion of the fund’s ETH to third-party validator operators. These operators run the software and hardware required to participate in Ethereum’s Proof-of-Stake consensus. When validators successfully propose and attest to blocks, the Ethereum protocol issues rewards in ETH that accrue to the fund’s staked balance.

From there, issuers use one of two approaches:

- NAV accretion, where staking rewards increase the per-share price over time.

- Сash distribution, where the fund periodically sells rewards for U.S. dollars and distributes cash to shareholders.

Grayscale uses the cash distribution method, paying out $9.4 million on January 6, 2026. BlackRock’s ETHB distributes 82% of gross rewards monthly.

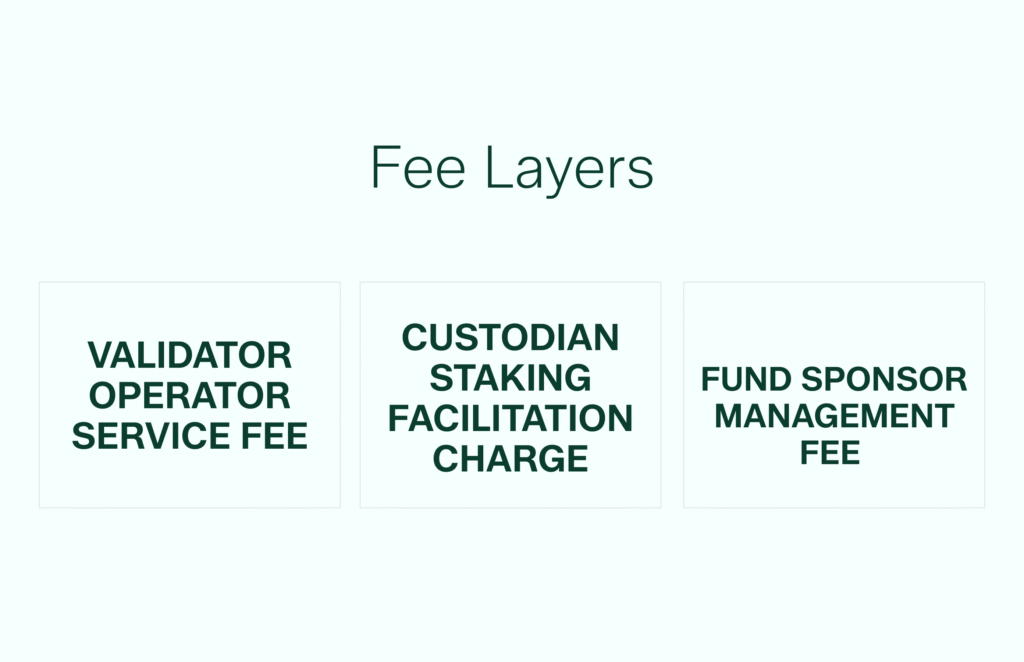

The rewards that reach shareholders are oftentimes net of multiple fee layers:

In a hypothetical case, at a gross Ethereum staking rate of approximately 3.2%, after all fees, holders of a product like ETHB may expect roughly 1.9% to 2.6% net annually. This net figure is what allocators should model against.

Ethereum enforces an unbonding period before staked ETH can be withdrawn, ranging from 9 to 50 days depending on network activity. ETFs cannot stake 100% of their ETH and still meet daily redemption obligations. This is arguably why ETHB stakes 70% to 95% of its holdings. The unstaked portion serves as a liquidity buffer.

Solana Staking ETFs: What’s Filed and What’s Pending

Solana staking ETFs represent the second major wave of staked crypto products in the U.S. and offer a useful comparison for Ethereum-focused allocators. Solana spot ETFs with built-in staking launched in late 2025, making them among the first U.S. ETFs to offer staked exposure from day one.

Bitwise’s Solana Staking ETF (BSOL) began trading on October 28, 2025.

- It stakes 100% of its SOL holdings through its Helius validator and reports net staking rewards of 7.20%.

- BSOL surpassed $500 million in managed tokens by January 2026 and captured roughly 98% of early Solana ETF inflows.

- The sponsor fee is 0.20% after a 3-month initial waiver period.

VanEck launched its Solana ETF (VSOL) on Nasdaq on November 17, 2025.

- VSOL uses SOL Strategies’ Orangefin validator for staking operations. The sponsor fee is 0.30%, which was fully waived (along with the 0.28% staking provider fee) for the first $1 billion in managed tokens or until February 17, 2026.

- Gemini serves as the primary custodian, with Coinbase Custody as an additional custodian.

Additional Solana ETF products have launched from Fidelity (FSOL), 21Shares (TSOL), Grayscale (GSOL), and Franklin Templeton (SOEZ).

- Grayscale renamed its product to Grayscale Solana Staking ETF on January 5, 2026.

- The category attracted 23 separate filings across issuers, with 6 products live by November 2025 and collectively generating over $4.6 billion in cumulative trading volume.

The key difference between SOL and ETH staking ETFs is the reward rate. Solana’s protocol runs at approximately 6% to 7% gross, compared to Ethereum’s 3.1% to 3.3%. For multi-asset allocators, the two categories offer a way to diversify across Proof-of-Stake networks with different risk and reward profiles.

Infrastructure Behind Staking ETFs

Behind every staking ETF is a stack of infrastructure that determines whether rewards are maximized and penalties avoided.

The typical structure involves three parties:

- the ETF sponsor (e.g., BlackRock),

- the qualified custodian (e.g., Coinbase Custody or Anchorage Digital),

- and the validator operator.

The custodian holds the ETH, the validator operator runs the consensus nodes, and the sponsor sets the allocation policy.

Validator operations require 24/7 uptime. When a validator goes offline, it misses block proposals and attestations, reducing rewards. If a validator behaves improperly (e.g., double-signing or extended downtime), the Ethereum protocol can “slash” the staked ETH, permanently destroying a portion of it as a penalty. For ETFs, any slashing event reduces the fund’s NAV and is shared across all shareholders.

This is where institutional-grade staking providers become critical.

- Everstake has operated validator infrastructure across 130+ Proof-of-Stake networks, securing billions in staked value.

- The company maintains a 99.98% observed uptime across all supported networks using geo-distributed bare-metal infrastructure with automated failover.

- Everstake holds the full-stack compliance certification suite in the validator industry: SOC 2 Type II, ISO/IEC 27001, NIST CSF, ITGC, GDPR, and CCPA.

- Everstake operates on a fully non-custodial basis, meaning the institution retains control of private keys and withdrawal addresses at all times. Our infrastructure integrates natively with leading custodians, including BitGo, Anchorage Digital, Zodia Custody, Copper.co, and Safe.

- The combination of compliance certifications, an uptime track record, and a history of zero material slashing on major networks provides the operational assurance that ETF-grade products demand.

As the number of staking ETFs grows, validator infrastructure selection will become a more visible differentiator between competing products.

Regulatory Landscape

The regulatory picture for staking ETFs shifted decisively in early 2026. The SEC and CFTC issued a joint interpretive release on March 17, 2026, that classified staking rewards from 16 named digital commodities (including ETH) as non-securities. This reversed the position taken by former SEC Chair Gary Gensler, who had instructed ETF issuers to remove staking from their filings in 2024.

The interpretive release stated that

“Participants in Protocol Staking Activities do not need to register transactions with the Commission under the Securities Act or fall within an exemption from registration in connection with these Protocol Staking Activities,”

adding that

“a digital commodity itself does not constitute any of the financial instruments enumerated in the definition of ‘security’.”

For ETF sponsors, this regulatory clarity removed the primary legal risk that had delayed the launch of staking products for over a year.

Alongside the staking guidance, the GENIUS Act (signed into law in July 2025) established a federal stablecoin framework that helped clear the broader regulatory runway for crypto products with economic features beyond simple price tracking.

The CLARITY Act (H.R. 3633), which passed the House in July 2025 with a bipartisan vote of 294 to 134, aims to establish comprehensive market structure rules for digital assets, including clear jurisdictional boundaries between the SEC and CFTC.

The Senate has been assembling its version of the bill, with White House crypto adviser Patrick Witt indicating in April 2026 that many previously contentious issues have been resolved.

The practical effect for allocators is that staking within regulated ETF structures now has a firm legal basis in the United States.

Looking further ahead, the convergence of on-chain AI agents and autonomous delegation could reshape how staking ETFs manage validator selection and optimize reward rates in future iterations. As agent-based infrastructure matures, the operational layer beneath these funds will likely become more dynamic and responsive.

Frequently Asked Questions

What is a staking ETF?

A staking ETF is an exchange-traded fund that holds a Proof-of-Stake cryptocurrency (such as ETH or SOL), stakes a portion of those holdings to participate in network validation, and passes the resulting rewards to shareholders. It combines price exposure with network-level economic participation in a single regulated wrapper.

Do staking ETFs pay a distribution?

Yes, but the method varies by issuer. Grayscale’s ETHE converts staking rewards to cash and distributes them periodically. BlackRock’s ETHB distributes 82% of gross staking rewards to shareholders monthly. Some products may instead accrete rewards into the fund’s NAV, increasing per-share value rather than paying cash. Check each fund’s prospectus for specifics.

How does ETHB differ from ETHA?

ETHA is BlackRock’s spot-only Ethereum Trust ETF, holding ETH in cold storage and tracking the price of Ether. ETHB is the iShares Staked Ethereum Trust ETF, which additionally stakes 70% to 95% of its ETH via Coinbase Prime and distributes staking rewards. ETHA charges a 0.25% sponsor fee. ETHB charges the same sponsor fee plus retains 18% of staking rewards for operational costs.

What is the risk of slashing in a staking ETF?

Slashing occurs when a validator violates protocol rules (such as double-signing or prolonged downtime), and the Ethereum network penalizes the staked ETH by destroying a portion of it. In a staking ETF, any slashing penalty reduces the fund’s total holdings and is reflected in a lower NAV. Fund managers mitigate this by selecting validators with strong uptime records and distributing staked ETH across multiple operators. The risk is low but not zero.

Are staking ETF distributions taxable?

Staking distributions from ETFs may be treated as taxable events. The specific tax treatment depends on how the fund structures its distributions and the shareholder’s jurisdiction. The U.S. Treasury and the IRS issued guidance in late 2025 that provides greater clarity on the taxation of staking rewards for exchange-traded products. Consult a qualified tax advisor for guidance on your specific situation.

Can I stake ETH directly instead of using an ETF?

Yes. Direct staking offers more control over validator selection and avoids fund-level fees. However, it requires a minimum of 32 ETH (approximately $55,000 to $70,000 at current prices) to run a solo validator, plus the technical expertise to maintain 24/7 uptime. Staking-as-a-service providers like Everstake lower the technical barrier while maintaining non-custodial security. An ETF suits allocators who want staking exposure within a regulated, brokerage-accessible structure without managing operations directly.

Which Ethereum staking ETFs are available in the U.S. today?

As of April 2026, two are live: Grayscale Ethereum Staking ETF (ETHE) and BlackRock iShares Staked Ethereum Trust ETF (ETHB). Pending staking amendments from Fidelity, Franklin Templeton, Invesco, 21Shares, and VanEck are expected to be approved in Q2 2026. The Grayscale Ethereum Staking Mini ETF (ticker: ETH) also offers staking exposure at a lower fee point of 0.15% with over $1.2 billion in managed tokens.

Disclaimer:

This guide is provided for informational purposes only and does not constitute legal, financial, tax, or investment advice. The information contained herein reflects the state of applicable regulations and market practices as of the date of publication and is subject to change without notice. Readers should not rely on this material as a substitute for independent professional advice tailored to their specific circumstances.

The regulatory analysis in this guide is provided as general background only. Compliance obligations vary by jurisdiction, entity type, and individual facts. Institutions should consult qualified legal and compliance counsel before making any decisions relating to staking arrangements, custody models, or regulatory status.

The information provided is not intended for recipients residing in the United Kingdom.

Share with your network